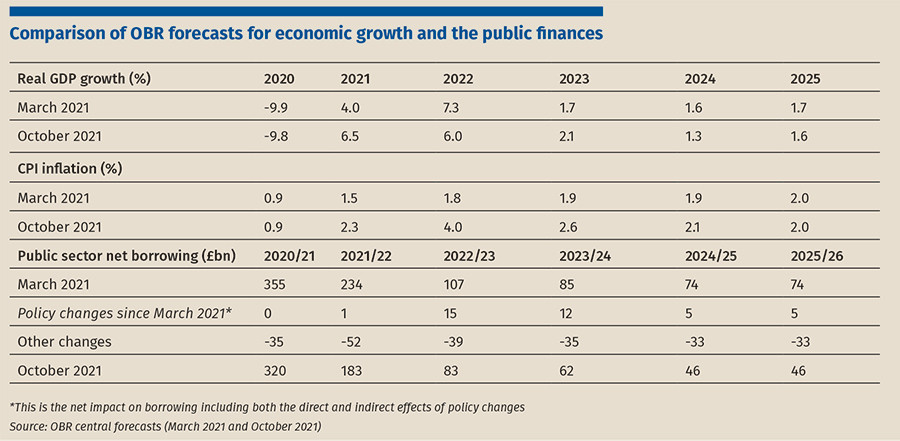

In this Budget, the chancellor benefited from favourable revisions to the latest Office for Budget Responsibility (OBR) forecasts for economic growth, reflecting the stronger recovery already seen in the spring and summer. As the table (below) shows, UK GDP growth is now expected to be around 6.5% in 2021, as compared to the 4% expected by the OBR in March.

Beyond the current year, real GDP growth is not expected to be higher on average than forecast in March, but the good news earlier this year is sufficient for the OBR to have revised down its central estimate of the longer term ‘scarring’ to the UK economy due to the pandemic from 3% to 2% of GDP. This implies a larger economy in the long run and higher tax revenues, reducing public borrowing by around £15bn per year by 2025.

The other major forecast change is that inflation is now expected to be much higher than in the OBR’s March forecast both this year and for the next two years, peaking at an annual average of 4% in 2022. This is bad news for household finances, but higher inflation has more mixed impacts on the public finances since it implies both higher tax receipts in cash terms and higher public spending.

Allowing for other forecast changes, public borrowing is now expected – excluding the impact of tax and spending changes since March 2021 – to be £33bn lower in 2025/26 than the OBR estimated in March. This gave the chancellor more room for manoeuvre while still keeping to his fiscal rules of borrowing only to invest and getting the ratio of public debt to GDP back on a declining path in the medium term.

In the event, there have been significant policy changes since March 2021, although the biggest of these was pre-announced last month with the new health and social care levy and corresponding increases in planned public spending in these areas. The October Budget added some further changes to both tax and public spending, though generally involving smaller sums of money despite a long list of announcements in the lead up to the Budget and during the speech itself.

Overall, the net direct and indirect impact of policy changes since March 2021, as shown in the table, is to boost public borrowing by around £15bn in 2022/23 as higher public spending outweighs tax increases. But this net impact declines to only around £5bn in 2024/25 and 2025/26 as further tax increases come through.

The OBR now estimates that total tax receipts will rise from 33.5% of GDP before the pandemic in 2019/20 to 36.2% by 2026/27, the highest since the early 1950s. The three major drivers of this upward trend are higher corporate tax rates from April 2023 onwards, frozen income tax allowances and thresholds over the next few years and the new health and social care levy. Announcements in the October Budget of cuts in business rates, alcohol duties and some other giveaways were small beer by comparison.

The positive side of this higher tax level is the ability to spend more on public services. The NHS is by far the largest beneficiary but there will also be significant additional funds over the next three to four years for schools, social care, defence and transport infrastructure. Overseas aid is also set to return to 0.7% of GDP from 2024/25 based on current OBR forecasts.

In part, this is the inevitable result of the pressures of an ageing population on public spending in areas like health, social care and state pensions. But the government has also made a strategic choice not to return to the era of austerity on public spending, which inevitably implies higher taxes.