The Finance Bill committee stage debate removed a majority of the Finance Bill following discussions with the opposition party.

This was in line with a call by CIOT in a letter to the chancellor, sent last week, in which CIOT President Bill Dodwell warned of the risks of rushing through a large number of tax changes without any real parliamentary scrutiny.

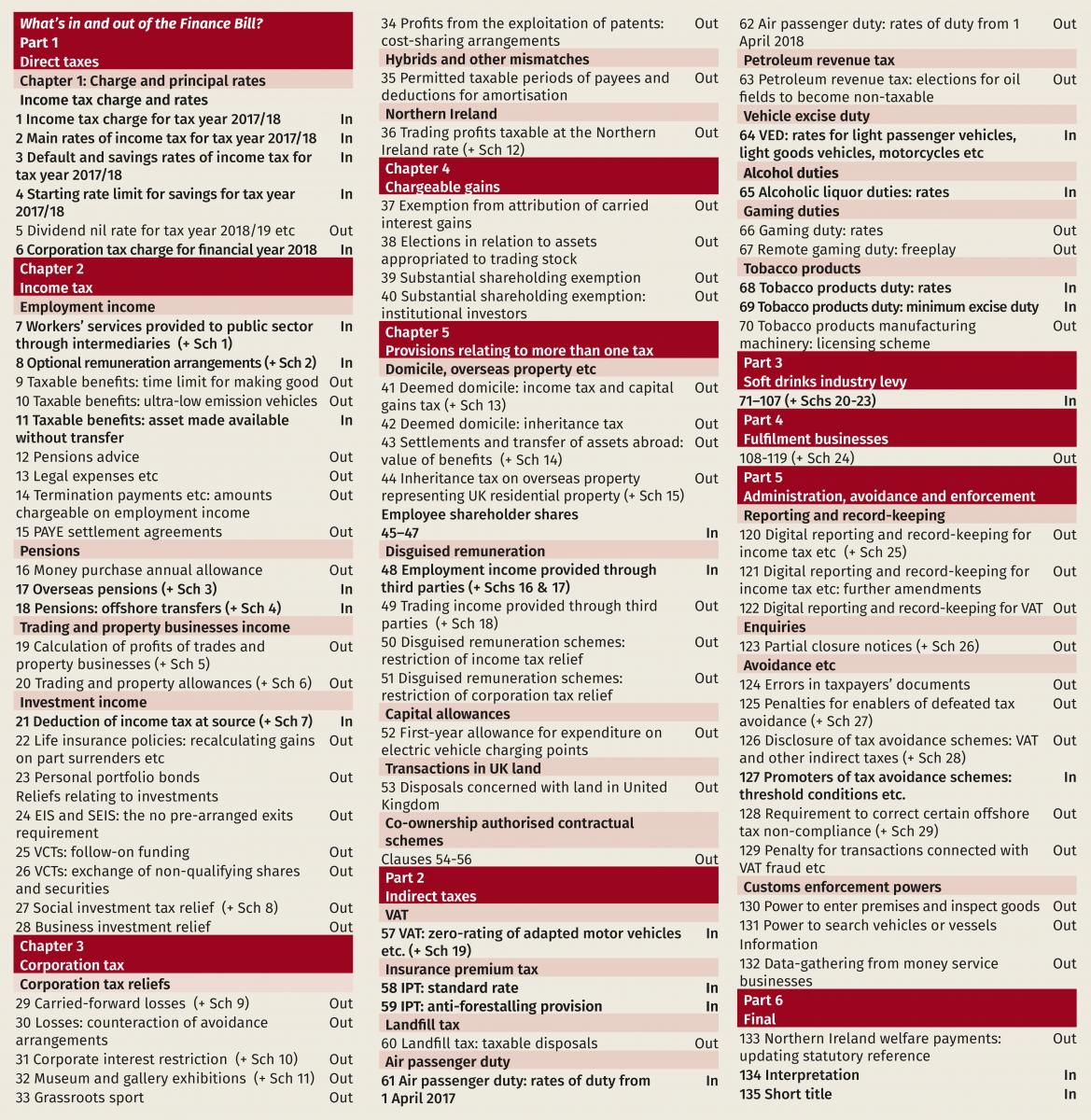

Clauses dropped include those on making tax digital, corporate loss relief and interest deductibility, VAT in relation to fulfilment houses and penalties for enablers of defeated tax avoidance schemes. It is likely that most if not all of the provisions dropped will return in a Bill after the election, regardless of who wins the election.

The Committee stage debate was limited to just four hours on Tuesday 25 April.

While this isn’t an ideal way to take a Finance Bill through Parliament, the government and opposition both deserve praise for agreeing to take the most controversial and/or complex provisions out of the Bill so they can get the further scrutiny they merit when Parliament returns after the election.

What is in and what is out of the Bill is shown in the table below.

Also worth noting is that the government has tabled some amendments. Leaving aside a few related to clauses being deleted from the Bill, these cover:

Home >Articles > What’s in and what’s out of the Finance Bill?

What’s in and what’s out of the Finance Bill?

The Finance Bill committee stage debate removed a majority of the Finance Bill following discussions with the opposition party.

This was in line with a call by CIOT in a letter to the chancellor, sent last week, in which CIOT President Bill Dodwell warned of the risks of rushing through a large number of tax changes without any real parliamentary scrutiny.

Clauses dropped include those on making tax digital, corporate loss relief and interest deductibility, VAT in relation to fulfilment houses and penalties for enablers of defeated tax avoidance schemes. It is likely that most if not all of the provisions dropped will return in a Bill after the election, regardless of who wins the election.

The Committee stage debate was limited to just four hours on Tuesday 25 April.

While this isn’t an ideal way to take a Finance Bill through Parliament, the government and opposition both deserve praise for agreeing to take the most controversial and/or complex provisions out of the Bill so they can get the further scrutiny they merit when Parliament returns after the election.

What is in and what is out of the Bill is shown in the table below.

Also worth noting is that the government has tabled some amendments. Leaving aside a few related to clauses being deleted from the Bill, these cover:

2e57498c-0da6-4646-a5fb-7a7570a14975.tmb-editorspic.jpg?sfvrsn=3909c9d0_1)