When Mr Sunak announced measures to help the self-employed on 26 March 2020, he pointedly noted that it was hard to justify the fact that self-employed persons pay lower national insurance contributions (NICs) than employees:

‘If we all want to benefit equally from state support, we must pay in equally’. The growth in the self-employed population in recent years relative to the number of employees has deprived the exchequer of a substantial amount of NICs receipts.

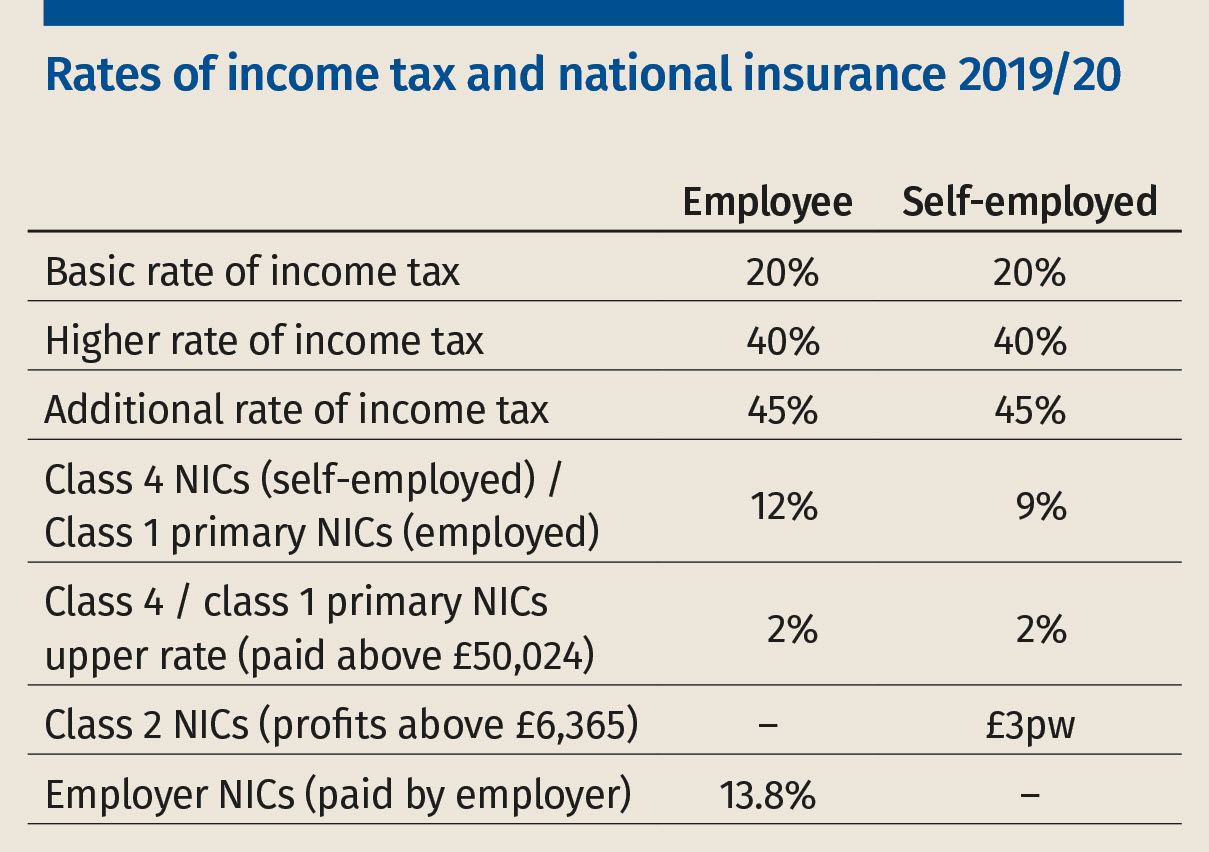

The historic discrepancy between the amount of NICs payable by those who are employees and those who are self-employed is due to the fact that until recently the self-employed were eligible for less state benefits than employees. The self-employed were not eligible for the same contributory welfare benefits and statutory payments as employees; nor were they eligible for the state second pension.

But this gap has been eroded by policy changes in recent years. In particular, the introduction of a ‘single-tier’ state pension for people who reach state pension age on or after 6 April 2016 has given the self-employed exactly the same state pension as employees, even though they pay substantially less NICs on their earnings than employees. The differences in eligibility for state benefits between the employed and self-employed are now mainly limited to certain parental benefits, e.g. statutory maternity pay.

Chancellor Philip Hammond attempted to reduce the gap between the NICs paid by the self-employed and employees in his Spring Budget 2017. The Budget documentation (National insurance and the self-employed factsheet) highlighted that the NICs foregone as a result of the lower rates paid by the self-employed compared with employees is estimated to have cost the public finances £5.1bn in 2016/17 (the figure is substantially higher now). As quid pro quo for increasing the NICs payable by the self-employed, he said that he would consider whether there was a case for greater parity in parental benefits between the self-employed and the employed.

But Mr Hammond had to abandon his attempt to reform NICs in the face of a threatened revolt by Tory backbenchers at a time when the government only had a small majority in parliament. It remains to be seen whether Rishi Sunak, as a member of a Tory government with a strong majority, succeeds in introducing this long overdue reform of the NICs paid by the self-employed in a future budget. Some Tory backbenchers have predictably reacted in fury against his suggestion that the self-employed might have to pay a fairer amount of NICs for the benefits they enjoy (‘David Davis slams Chancellor Rishi Sunak’s "tax raid" on self-employed’, Daily Mail, 28 March 2020).

Hoist by their own petard?

Owner-managers of small companies who pay themselves mainly through dividends rather than wages or salaries have found themselves hoist by their own petard. They will not be eligible for the emergency income support that will be paid to employees or the self-employed. The Financial Times reported (27 March 2020) that Treasury officials have intimated that the owners of incorporated small businesses who pursue ‘dividend strategies’ don’t deserve support because they have been engaging in tax avoidance.

This suggests that the new chancellor is unlikely to be sympathetic to extending the recent deferral of IR35 reform beyond 2021. He might also be prepared to consider increasing the rate of income tax paid on dividends, or the introduction of a NICs charge on dividends paid in lieu of remuneration by personal service companies to avoid the payment of employee and employer NICs, or both measures. (A principled case could also be made for ending the blanket exemption from NICs of pensioners. It would not be unreasonable to impose NICs on their earnings, given that some 40% of pensioners are employed or self-employed.)

Previous chancellors have shied away from imposing NICs on dividends because it is not easy to distinguish between the element of dividends that represent the passive return from the capital invested, and the element that reflects the fruits of the labour of the owners of the company. Officials are likely to advise the chancellor that it is possible to devise rules to divide a small company’s dividends between the reward for capital and labour supply, but that it would be controversial and involve some administrative complexity.

The restrictions on the level of support available to help maintain the level of the income of employees and the self-employed are understandable. But the delay in the announcement of specific measures to help those on low incomes from self-employment who don’t file annual SA returns because of their low incomes is regrettable. According to HMRC statistics published earlier this year, the number of people required to file SA returns was at a record high even before the Covid-19 crisis, because of the rapid growth in the number of self-employed persons, especially in the ‘gig economy’.

In practice, many self-employed persons fail to submit SA returns. Strictly speaking, all self-employed persons have to complete SA returns, unless their trading, casual or miscellaneous income is under £1,000 and therefore exempt because it is below the trading allowance. Some people deliberately fail to comply in order to evade tax. Others do so inadvertently, as a result of their mistaken belief that they don’t have to return details of their trading income if it is below the level of their (unused) personal allowances.

The taxpayers in the latter category often don’t bother to quantify the precise amount of their income. But they will pay dearly for their ignorance of, or failure to comply with, the law. They will find it impossible to claim income support under the new scheme unless they have retained their records and they can secure help to compute their income to submit SA returns for earlier years.

Many of these people are reliant on their small incomes to survive. The government should provide additional funding to the tax charities, and it should support the efforts of professional advisers to encourage such taxpayers to submit their tax returns to enable them to claim income support. They are more likely to receive timely financial support from the HMRC-administered scheme than they are to receive it under the universal credit scheme operated by the hard-pressed Department for Work and Pensions.

In the end, we’ll all pay more...

All taxpayers will experience the final sting in the tail in the chancellor’s new measures. We will all have to bear our share of not just the extra spending of £30bn announced in Budget 2020, but also the massive open-ended cost of the Covid-19 emergency measures. Paul Johnson, the director of the Institute for Fiscal Studies has remarked: ‘If we get out of this with a fiscal deficit of much less than £200bn next year, we’ll be lucky. Debt as a fraction of national income will ratchet sharply upwards. Disruption to education, to supply chains, almost certainly to mental health, will have long-term consequences’ (The Times, 30 March 2020).

The Bank of England’s announcement of some £200bn of additional ‘quantitative easing’ and reduced interest rates will also have profound economic consequences for taxpayers. The Bank has made an open-ended promise to provide further liquidity, and to purchase gilts, commercial paper and even shares, comparable to the government’s commitment to offer the NHS practically unlimited funding to deal with the crisis. Since the government has guaranteed the Bank’s credit and monetary bonanza, it could end up burdened with as much, if not more debt than after the financial crisis.

Even with interest rates at 0.1%, the repayment of public debt has to be financed through taxation; it has to be carefully managed to avoid crowding out the demand for finance by commercial firms. The massive expansion of money and credit in the economy will initially lead to asset price inflation, which will benefit the most wealthy, and then stoke up inflationary tendencies after the current crisis ends and the economy begins to pick up.

It is impossible to predict exactly when the current health crisis will end. But it is clear from the daily failures of large and small businesses that it will leave the economy severely depressed, if not devastated. The Centre for Economics and Business Research has forecast that the British economy could contract by 15% between April and June 2020; in contrast, the economy shrank by 2.2% during the nadir of the 2008 financial crisis. The government will come out of the crisis with substantially higher debt and dramatically reduced tax revenues. It will have to increase tax rates or introduce new taxes or both, and to use fiscal policy to curb the incipient surge in price level inflation created by the Bank of England’s expansionary monetary policy.