What are the ORIP rules? What are they seeking to achieve?

It is perhaps surprising that so little has been said about the offshore receipts in respect of intangible property (ORIP) rules. After all, these are internationally unique, transformed materially in scope during the consultation process and are very widely drawn. They were also introduced into law on 6 April 2019, despite the government acknowledging (before royal assent) that the rules had triggered widespread concern and had ‘unintended outcomes’ that needed to be fixed. That the government sees a need for legislation is clear; whether this is the way to address that need seems questionable.

The ORIP rules began as a withholding tax proposal in a 2017 consultation, aimed at base erosion by targeting ‘a narrow range’ of intra-group arrangements that achieve an artificially low effective tax rate through royalty payments to companies holding IP in low tax jurisdictions. Responses to that consultation pushed hard against the proposal, especially the use of a withholding tax.

Be careful what you wish for. The ORIP legislation, found in ITTOIA 2005 Part 5 Chapter 2A, introduced an income tax on gross receipts rather than a withholding tax; however, it does not require a UK nexus beyond UK sales, is not limited to intra-group arrangements and is only subject to a pretty malnourished set of exclusions.

The policy has also moved to the broader aim of discouraging multinational businesses from holding intangible property in low tax jurisdictions, instead of the jurisdictions where the substantive economic activities relating to that intangible property are located. This goes beyond protecting the UK tax base from profit shifting to offshore jurisdictions. It is redefining the concept of how much tax should be paid and on what portion of profits, or rather revenue, in the UK.

While the ORIP rules are not limited to digital businesses, there is a clear overlap with both of the two pillars being considered by the OECD/G20 to address tax challenges from the digitalisation of the economy (a roadmap for resolution of this was published on 31 May 2019 (see bit.ly/2Wz9t7B)).

Is the policy underpinning the legislation important? Well, yes. It should inform the (ongoing) consultation process to improve the rules; it guides how the legislation should be interpreted and applied; and, fundamentally, it supports or undermines the legitimacy of the rules.

How do the rules work?

The legislation that came into effect on 6 April 2019 was unchanged from the initial draft published in Finance Bill 2019 following the response to the 2017 consultation (the ‘response document’). The rules are as discussed in ‘The new income tax charge on ORIP’ (Steve Edge & Dominic Robertson, Tax Journal , 28 November 2018). By way of brief recap, there is a tax charge on ‘UK derived amounts’ arising in the tax year where a person:

The tax is due from any person who is resident outside the UK or a ‘full treaty territory’ (which requires a double tax treaty containing a non-discrimination provision). However, there is a wide secondary tax provision that can be used against one or more connected persons, with very limited appeal rights.

An amount is ‘UK-derived’ if it is in respect of the enjoyment or exercise of ‘intangible property’, and that enjoyment or exercise ‘enabled, facilitated or promoted’ ‘UK sales’, being the provision of services, goods or other property in the UK or to UK persons.

The exemptions have (deliberately) narrow scopes and there is a wide reaching, arguably punitive, TAAR back to Budget day 2018.

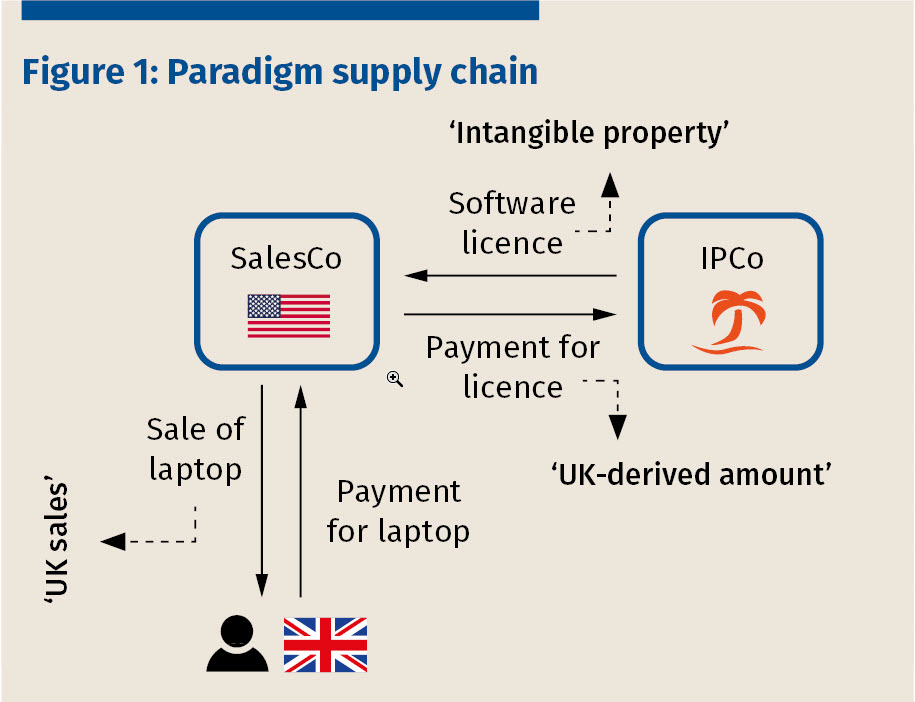

The paradigm supply chain that is targeted by the measure is shown in figure 1.

The government has a regulation-making power to amend the ORIP rules until 31 December 2019, perhaps recognising the legislation’s known flaws. The first draft statutory instrument (the ‘draft regulations’) has just been published for consultation, together with draft guidance. In the authors’ view, the draft regulations only partly address these flaws and fall significantly short of expectations.

The remainder of this article seeks to illustrate who should worry about these rules and why, by concentrating on four critical areas that businesses should be aware of and which we believe need to be fixed by the draft regulations as a priority.

Does ‘intangible property’ only apply to intellectual property rights?

Conceptually, the ORIP regime appears to be focused on intellectual property.

The original withholding tax version targeted base eroding intra-group royalty payments in large groups. In switching to the ORIP charge, the response document maintained that it would be levelled at payments ‘that are referable to intellectual property or rights over other intangible property’, such as royalty and distribution payments.

The draft guidance describes the regime as being aimed at encouraging intangible property to be owned in a fully taxed jurisdiction where the property is ‘developed, enhanced, managed, protected and exploited’. Despite the reference to intangible property, this phrasing clearly contemplates the exploitation of a standalone asset in the form of intellectual property or similar rights, and the examples cited (such as goodwill and trademarks) are in line with that interpretation.

The measure, as proposed and enacted, targets value generating assets which have been consciously located in a low tax jurisdiction and could justify (on a transfer-priced basis) value being allocated outside the UK.

However, this narrow ambit has been abandoned in the definition of ‘intangible property’, which does not so much tell you what it is but what it is not. Intangible property is any property not falling within specific exclusions for tangible property, land, shares and financial assets (like loan relationships). There is no link back to some concept of intellectual property. This means that payments not targeted by the policy are caught by the regime, such as those in respect of contractual rights like deferred or unascertainable consideration and management service payments.

The government reasons that this is needed to future proof the legislation for unanticipated commercial or technological developments, and to stop multinationals side-stepping the rules. There is some merit in this, although there is rather less in the government’s other justification that the measure is ‘narrowly targeted in other ways’.

What is difficult to deny is that the regime will impose a heavy compliance burden on taxpayers to identify whether the regime applies, and it is very likely that payments outside the intended ambit of the regime will be subject to tax under it. As has happened elsewhere in the regime, the government has deliberately stepped outside its real policy aim in order to comprehensively counter perceived future tax avoidance risks.

In the authors’ view, the government should correct this misstep in the current draft regulations and redefine intangible property to align it more closely with intellectual property rights, perhaps by using the definition of ‘royalty’, together with other payments for the use or exploitation of rights over ‘intellectual property’, in both cases as already defined for the purposes of ITA 2007 Part 15. The government could reverse the regulation making power and have a power to add limbs to this specific definition (with retrospective effect where necessary). This would allow it to counter identified avoidance or future commercial or technological developments without sacrificing certainty and fairness in the process.

What UK nexus is required? When will intangible property ‘enable, facilitate or promote’ UK sales?

An amount in respect of intangible property rights is only a ‘UK-derived amount’ if enjoyment of those rights ‘enables, facilitates or promotes’ UK sales directly or indirectly. This ‘enables’ test is therefore key to limiting the scope of the UK-derived amount to the payments attributable to the exploitation of that intangible property in the UK that the ORIP regime is intended to target.

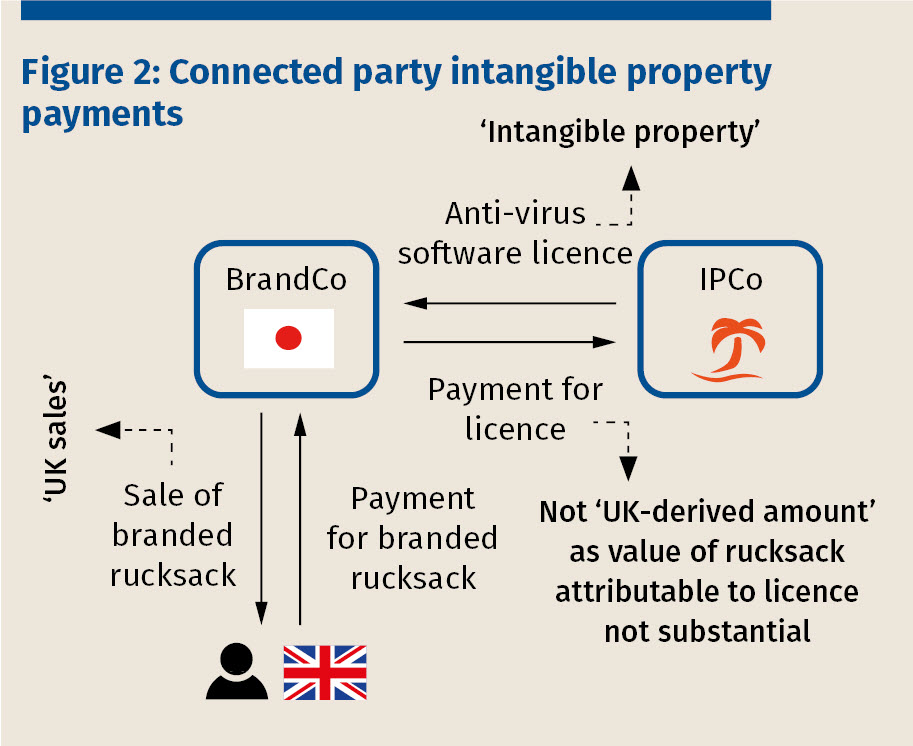

The response document stated that the measure was intended to apply to income in respect of intangible property that is ‘substantially exploited’ in the UK market. This was echoed in the examples (such as example 8, a simplified form of which is depicted in figure 2 below), which make it clear that the measure would not apply unless a ‘substantial’ amount of the value of the good or service being sold in the UK is attributable to the value of the intangible property in question. It seemed that this substance requirement was to be read into the ‘enables’ test – perhaps on the basis that intangible property could not have enabled, facilitated or promoted sales unless it played a substantial part in those sales. The government was encouraged to make this clear in the legislation for certainty.

Instead, the proposed new s 608GA will disregard amounts from being UK-derived amounts if they arise from UK sales by a third party which are enabled, facilitated or promoted ‘to an insignificant extent’ by the intangible property rights in question. This measure seems to give with one hand and take away with the other:

The authors cannot see any policy reason to differentiate between third party and connected party arrangements in this respect, and consider that the government should replace the disregard with the addition of a positive substance requirement for s 608F.

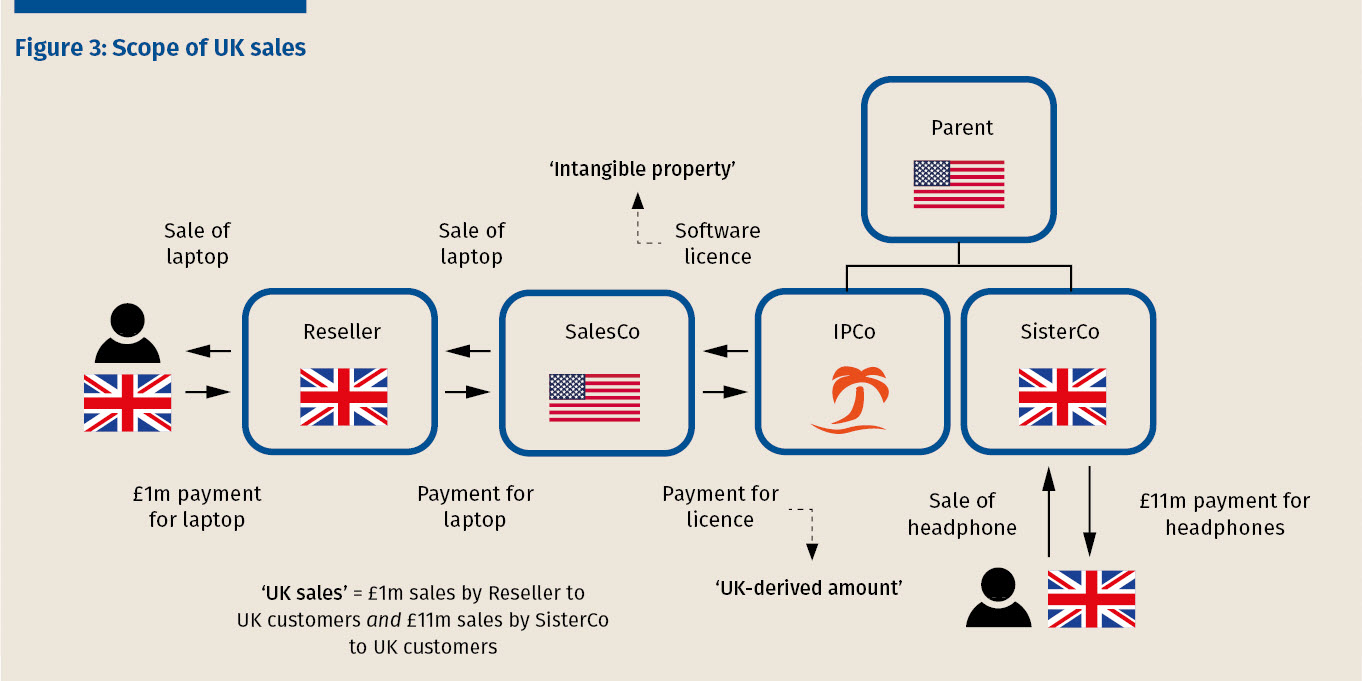

One positive change in the draft regulations is the insertion of a new interpretation provision in s 608F to the effect that where property is resold without change, such as by resellers or retailers, that intermediate sale (like the sale by SalesCo to Reseller in figure 3) is not a ‘UK sale’ (and therefore any intangible property payment in respect of that intermediate sale is not a UK-derived amount). This is a narrowly drafted provision but should assuage concerns about supply chains which pass through the UK before an ultimate sale outside the UK being tainted, provided that the ‘no change’ requirement is fully satisfied.

Can I rely on the exemptions?

The decision to have wide charging provisions has not been counterbalanced by appropriate exemptions to target the scope of the regime properly. Although the government has exercised its regulation making power to propose more exemptions in the draft regulations, the existing and proposed exemptions are together still deliberately very narrow.

The government acknowledges that the exemption in s 608K (where business is undertaken within a territory of residence) will rarely (if ever?) apply; and that, as the proposed new exemption for taxpayers in yet to be specified territories is a policy concession, it must be tightly controlled. Therefore, we will focus on the other exemptions which the government, if so inclined, could make more useful in practice.

Section 608J imposes a de minimis threshold so that a charge does not arise if the total value of UK sales made by the taxpayer and any of its connected persons does not exceed £10m. The purpose of the threshold is to shift both the compliance and the tax burden of the ORIP regime away from small businesses and towards large multinational groups. This is a fair objective, but it has been actioned in a way that significantly undermines its usefulness.

UK sales (including third party UK sales) are included if the taxpayer (or its connected persons) receives an amount relating to those UK sales. One problem is illustrated in figure 3: is it commercially realistic to expect Reseller to be willing to provide UK sales information to the third party SalesCo, let alone to an unconnected offshore IPCo?

Further, the test counts all UK sales and not only those with some connection to offshore intangible property. The de minimis is not limited to a group’s UK sales relating to UK-derived amounts. All UK sales by anyone connected with the offshore intangible property holder must be counted, even if made by a different division of the group which does not rely on any intangible property for its sales. It is unclear whether the government intends this result (which, as exemplified in figure 3, seems arbitrary).

The authors consider that there should be a de minimis threshold for UK-derived amounts, in addition to one for UK sales: from a compliance perspective, different groups may find different thresholds less burdensome. Further, any UK sales relating to UK-derived amounts disregarded under s 608GA (where intangible property makes an insignificant contribution) should not be UK sales for the purposes of calculating the de minimis (as is the case for resales falling within the amended s 608F).

This exemption (s 608L) is only available if at least half of the amount of UK tax that would be charged on the UK-derived amount under the ORIP rules is paid in the territory of the taxpayer. As drafted, this exemption will rarely apply because:

it only takes into account taxes in the (low tax) territory of the taxpayer and ignores other taxes that are paid (inside or outside the UK) in respect of the UK-derived amount, such as withholding tax and CFC or equivalent charges; and

it compares a tax on gross income (ORIP) with taxes (if any) on net income.

The draft regulations propose a new exemption (s 608MB) to address double taxation within the ORIP rules but not double taxation risk generally. Its purpose is to ensure that the same UK-derived amount is not taxed more than once in the same group (such as under sub-licensing arrangements) under the ORIP regime.

A new rule (ITA 2007 s 918) is also proposed to switch off any UK withholding tax on an amount to which an ORIP charge applies.

Both of these measures are welcome, but the government should extend s 608MB to cover:

Without addressing the issues identified above for ss 608L and 608MB, economic double taxation and compliance burden concerns will remain, which in turn will raise questions as to whether the government is complying with its international obligations.

Why is the TAAR punitively unfair?

As is universally the case for new tax legislation, the ORIP regime includes (with effect from 29 October 2018) a broad TAAR which can be used to counteract any arrangements which have a main purpose of seeking to avoid the ORIP tax charge. What was unexpected (given that the policy aim was to discourage multinational groups from holding intangible property in low tax jurisdictions) is that group restructurings to transfer offshore intangible property to the UK or a full treaty territory will on the face of it fall foul of the TAAR.

The draft guidance makes clear that the government intends to use the TAAR to counteract the transfer of intangible property to the UK or any full treaty territory if any of a non-exhaustive set of factors are met, including if the transferee does not have any substantial operations in its jurisdiction or the substantive economic activity underlying the intangible property is undertaken elsewhere. This raises a few difficult points:

What next?

Multinational groups with a presence in offshore jurisdictions other than full treaty territories should take heed. They must consider whether any revenue or capital amounts received in those jurisdictions since 6 April 2019 relate to the widely defined ‘intangible property’. If so, they face the unenviable burden of working through the rules to determine how (and if) they can find a way out of an ORIP charge.

Given the significant compliance burden and the real economic double taxation risk that the ORIP regime poses, the government should reconsider its policy mission creep and whether too many who fall outside the real target areas will be adversely affected. It can only be hoped that sooner rather than later the government will avail itself of the opportunity presented by the draft regulations to cast the ORIP net more narrowly.