The Office of Tax Simplification has published its first review of the tax charges and reliefs which arise though the various stages in the lifecycle of a typical business. The picture which emerges is one in which well-intentioned reliefs and features combine to produce a very complex experience for those starting and growing a business, with plenty of opportunity for simplification. The ‘user experience’ lies at the heart of this review and if, as a result of this report, those running a business could spend more time on their business and less time on tax, the review will have been successful.

The Office of Tax Simplification (OTS) is the independent adviser to the chancellor on ways of simplifying the tax system. Based in HM Treasury and working closely with HM Treasury and HMRC, the OTS carries out independent research and, on the basis of the evidence, makes recommendations for simplification.

Most previous reviews have focused on a particular tax or a particular issue. For example, the recently published report on VAT was a first review of this particular tax. However, it was felt that there would be value in looking, for the first time, at all taxes across the whole of the business lifecycle so that the interactions between the taxes and the impact of the tax systems through the lifecycle could be explored more clearly. Indeed, this has proven to be a very useful perspective and it has become clear that someone starting and growing a business faces a sustained pressure of complexity throughout the lifecycle.

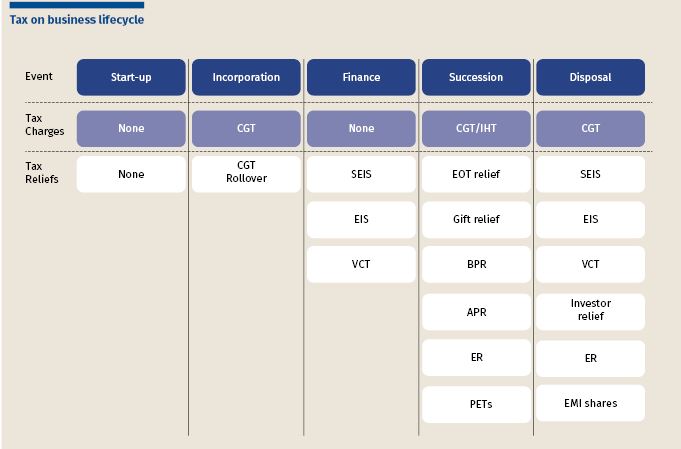

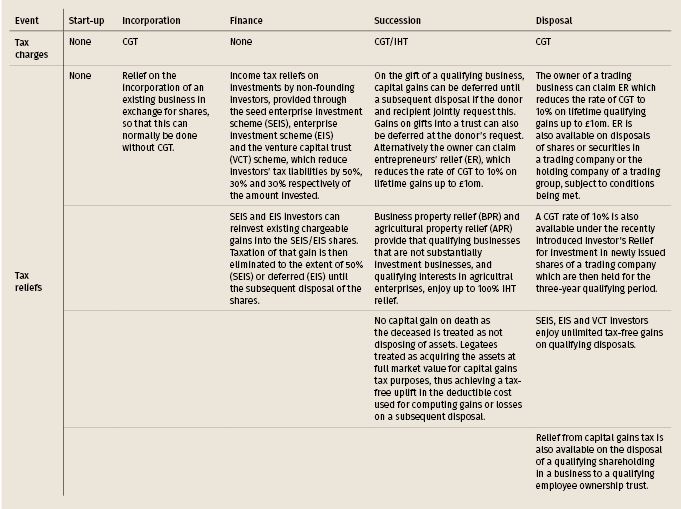

The various charges and reliefs are illustrated in the following charts. The key concern of the OTS is the ‘user experience’. How does it feel to the owner of the business and how much time and effort does he or she need to devote to understanding the tax issues? How intuitive are the concepts and the administrative requirements?

The UK is recognised as one of the best countries in the world in which to do business. Successive governments have been able to support businesses by providing tax reliefs to encourage innovation and investment and by ensuring that tax is not a hindrance at critical stages of business development; for example, by acting as a disincentive to potential reinvestment in innovation or by hampering successful transition through the business lifecycle. UK businesses raised more than £7.1bn in venture capital in 2016 and the UK is home to half of the top ten fastest growing companies in Europe, is the number one European destination for inward investment and is ranked fifth in the Global Innovation Index. Having noted this, it is clear that there is still more work to be done.

At the outset, it is not always clear to individuals when they may need to register, or with whom, and for those starting a small incorporated business the administrative burden of having to register separately with Companies House and with HMRC could be reduced by introducing a ‘one-stop shop’. This was previously recommended in the OTS’s report Small company taxation review, and HMRC is developing a facility on Gov.uk, although it is not yet complete.

The OTS also noted, in passing, that while there are reliefs for those raising capital from third parties later in the business lifecycle, there is no tax relief for those having to raise start-up capital on day one, particularly where that capital has to be raised from relatives, as is often the case. However, is relief for start-up capital actually required, as presumably many family members would provide support anyway? And is streamlining the reliefs available at start-up with those available later really simplification? These are both good questions, perhaps worthy of further reflection.

There are several areas where tax complexity might add to the challenges of raising finance. Firstly, in order to qualify for entrepreneurs’ relief (the 10% capital gains tax rate on disposal of qualifying business assets), it is necessary to hold a minimum of 5% of a company’s shares. The OTS heard that some business owners felt discouraged from bringing in external venture capital to the extent that there was a risk that their shareholding could be diluted below this level. The government launched a consultation at Spring Statement 2018 which the OTS fully supports.

The three main tax-favoured venture capital schemes are the enterprise investment scheme (EIS), the seed enterprise investment scheme (SEIS) and venture capital trusts (VCTs). These have common features but also a number of differences which means that they attract different types of investors who invest for different reasons. Whether the motivations of the investors are quite aligned with the needs of the companies is not entirely clear and many businesses are either unaware of the reliefs or find them difficult to understand. At the same time, it is inevitable that the objective of targeting the reliefs appropriately will result in some complexity. However, there are opportunities to remove some of the inconsistencies and to explore ways of simplifying some of the administrative procedures. In addition, there are cases where a business may be caught out in one way or another and might find relief is denied or withdrawn unexpectedly. This is an area which is worth examining further.

When a business is disposed of by way of a gift, relief from CGT is potentially available under entrepreneurs’ relief or CGT gift relief: they offer the option of paying 10% now, or potentially paying at the full rate at a later point in time. These two reliefs are mutually exclusive, but determining which is better to claim depends on the future plans of the recipient of the gift, which will often be uncertain at the time the choice needs to be made. Some simplification of the interaction of the reliefs would help to make the choice clearer and simpler for all parties, including HMRC.

Capital gains tax reliefs (entrepreneurs’ relief and gift relief) are available in respect of transfers of shares in trading companies where the non-trading element of the business is not more than 20% of the whole. In contrast, IHT business property relief is available on transfers of a business, or shares in a business, where the non-trading element of the business (whether incorporated or not) is less than 50%. As well as the confusing effect that results from two different rules, this can lead to businesses adopting commercially unnecessary and complex structures to preserve their qualification for the reliefs.

Strikingly, the cost of entrepreneurs’ relief, the 10% capital gains rate on disposal of a qualifying business, is greater than that of any of the other reliefs considered in the report. While those other reliefs appear to be designed to encourage investment in young and growing businesses, or to preserve existing business from break-up in the event of succession, entrepreneurs’ relief does not seem to achieve either of those objectives. Its place in the range of reliefs, and its purpose, warrant a closer look.

Tax reliefs on sale are generally available in respect of consideration received at the point of sale, including any value attributed to contingent consideration. The reliefs are not available in respect of additional contingent consideration received and accounted for at some later point. This difference of treatment will influence business owners to sell for cash when a sale with the consideration being tied to future business performance might have been a better structure to encourage business growth. Simplifying the treatments by bringing them into line would remove a business distortion.

The ‘double taxation’ both of the sale proceeds of a business by a company, as well as the subsequent capital distributions when the company is wound up, is disadvantageous for the seller, compared to the single tax charge on the proceeds of sale of a company itself. In contrast, the purchaser of the business enjoys more favourable tax treatment and reduces their risks by buying assets from a company, rather than buying the company. A conflict of interest is therefore created between vendors and purchasers, which must make successful business transactions more difficult to achieve. Aligning the tax treatments would help to reduce such difficulties.

The OTS warmly welcomes comments and views from readers of Tax Journal. How should this work be taken forward? Clearly, there are some areas where the complexity is obvious, such as the venture capital reliefs. There are other areas, such as the possibility of relief for start-up capital, where the position is much less clear. Administrative aspects are clearly difficult for some businesses and the question, perhaps, is one of prioritisation at a time when HMRC is resource constrained by the demands of Brexit and making tax digital.

The availability of tax reliefs at various stages in the life of a business has evidently played an important part in creating a business climate that encourages entrepreneurial activity in the UK. However, the overall picture is complex and clearly confusing. Some of the reliefs are not as well known or understood as they might be. Is there more that the tax profession can do in this respect? If, as the OTS has found, some eligible businesses are simply not aware of the availability of some of the reliefs, their advisers might be more proactive in drawing these facilities to their attention. There are examples of businesses which have started to investigate a tax relief but found the process too difficult and it should be possible to learn from these experiences.

The need to encourage innovation and to support growing businesses, the economy and employment in the UK is a more vital priority than ever. The business tax system must be fit for this purpose and support these aims.

The OTS therefore suggests that there is a pressing need to undertake a detailed review of the tax system as it operates on key events in the business lifecycle, to help the UK economy to maximise its opportunities and to make the system clear and simple for companies to understand and use. This might be supplemented by additional work focusing on tax complexity as it impacts business growth, including learning from the OTS reviews of VAT and small company taxation.

We welcome views on the Business lifecycle report and thoughts on where the work might most helpfully be taken forward. We also welcome examples from practical experience and readers’ insights as to how some of the difficult areas might be approached. We plan to undertake further work in this area and readers’ views will be very useful in setting priorities.

Paul Morton and his OTS colleagues will be discussing the focus for tax simplification at a free event for tax professionals, in central London on the evening Wednesday 27 June. For more information and to reserve your place, click here