Shiv Mahalingham (Duff & Phelps) answers a query on the imminent notification deadline for the DPT.

Question

Should all companies with UK operations have considered the potential application of the UK diverted profits tax (DPT) regime or is it just companies with a particular profile that are caught? If I have not already done so, is it too late to file a Finance Act 2015 s 80 notification before the 30 June deadline?

Answer

The 30 June requirement is for companies with 31 December 2015 year ends, and it is those companies that should be considering the impending deadline. It is also likely that most companies with a year end of 31 December 2015 and that have an assigned HMRC customer relationship manager will already have been asked at some point over the past 12 months: ‘Could you please advise what conclusions have been drawn over the group’s exposure to diverted profits tax?’ If you have not received such a question through the risk assessment process and you have not already reviewed structures to assess whether a notification is required, then it may be worth considering the information below.

Reminder of the notification requirements

A section 80 notification (the involvement of entities or transactions lacking economic substance) could be required where: a provision is made or imposed between a UK resident company and a related person; the provision conveys on the UK resident company a tax reduction significantly greater than any tax increase for the other person (i.e. a ‘tax mismatch’); and it is reasonable to assume that the provision was designed to secure the tax reduction. The notification will not be required if:

at the end of the notification period, it is reasonable to conclude that no charge to DPT will arise for that period (ignoring the possibility of future transfer pricing adjustments);

before the end of the notification period, HMRC has confirmed that a notification is not required on the basis that sufficient information has been provided to determine whether to issue a preliminary notice and it has examined that information; or

at the end of the notification period, the taxpayer has concluded that it has provided HMRC with sufficient information to determine whether to issue a preliminary notice and that HMRC has examined that information.

Practical experience of when notification is required

Typical transactions and industries that we have analysed in the past 12 months and that may require notification include:

banks and insurance;

hedge funds;

leasing; and

other structures that have (historically) included the existence of a low tax jurisdiction.

In addition, the following (not so obvious) transactions have also required a review and notification in some isolated cases:

wholly UK based structures with trapped losses; and

entities not operating in low tax jurisdictions but operating under favourable tax regimes (e.g. tonnage tax, tax holidays, real estate investment trusts).

Note that in most of the above cases, there was a strong commercial rationale behind the transactions, which permitted a ‘no notification’ position to be adopted. However, this did require financial economic analysis to support the fact that there was a contribution to economic value that outweighed any incidental tax benefit, thereby supporting both the substance of the transaction and the fact that it was not designed to convey a tax benefit.

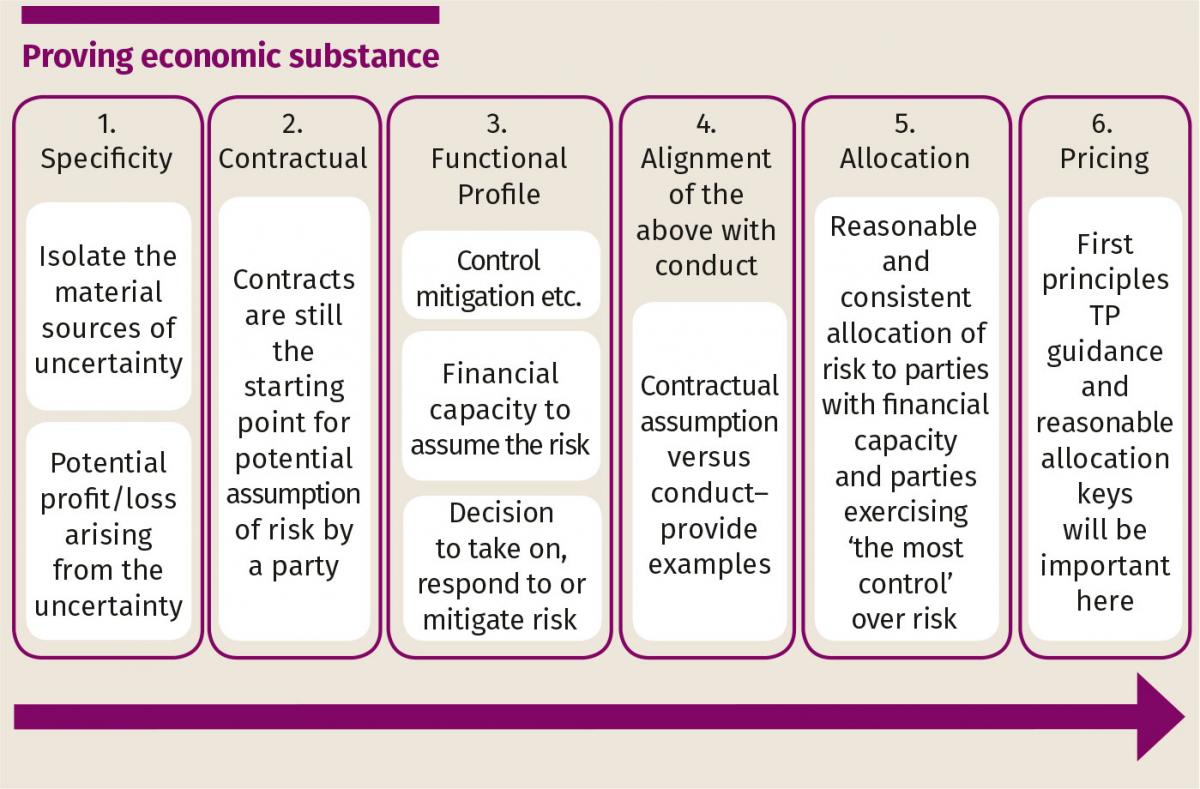

Proving economic substance has also been assisted by revised OECD transfer pricing guidelines relating to risk. These depart from the notion that substance requires bodies on the ground (an archaic concept for the industries listed above) in a welcome change to the OECD guidance (see figure below).

We have also had some experience of what ‘sufficient information’ means in this context. It is clear that groups that are under existing advance pricing agreements, and/or that have informal agreements with HMRC in relation to transfer pricing, have still had to enter into a new dialogue with HMRC to confirm this. (In the majority of cases that have hit my desk, this has been a straightforward process: advance pricing agreements or informal agreements are rarely sought if there is not a strong commercial fact pattern in place.) Groups that are still unsure could consider a discussion with HMRC through the risk assessment channels in the next week or so to mitigate any potential tax-geared penalties at a later date. A transparent discussion may require an allocation of resources; however, this may be more efficient in the long term when one considers a potential challenge from HMRC and also financial audit fees at a later date to backtrack and resolve an uncertain position.

Shiv Mahalingham (Duff & Phelps) answers a query on the imminent notification deadline for the DPT.

Question

Should all companies with UK operations have considered the potential application of the UK diverted profits tax (DPT) regime or is it just companies with a particular profile that are caught? If I have not already done so, is it too late to file a Finance Act 2015 s 80 notification before the 30 June deadline?

Answer

The 30 June requirement is for companies with 31 December 2015 year ends, and it is those companies that should be considering the impending deadline. It is also likely that most companies with a year end of 31 December 2015 and that have an assigned HMRC customer relationship manager will already have been asked at some point over the past 12 months: ‘Could you please advise what conclusions have been drawn over the group’s exposure to diverted profits tax?’ If you have not received such a question through the risk assessment process and you have not already reviewed structures to assess whether a notification is required, then it may be worth considering the information below.

Reminder of the notification requirements

A section 80 notification (the involvement of entities or transactions lacking economic substance) could be required where: a provision is made or imposed between a UK resident company and a related person; the provision conveys on the UK resident company a tax reduction significantly greater than any tax increase for the other person (i.e. a ‘tax mismatch’); and it is reasonable to assume that the provision was designed to secure the tax reduction. The notification will not be required if:

at the end of the notification period, it is reasonable to conclude that no charge to DPT will arise for that period (ignoring the possibility of future transfer pricing adjustments);

before the end of the notification period, HMRC has confirmed that a notification is not required on the basis that sufficient information has been provided to determine whether to issue a preliminary notice and it has examined that information; or

at the end of the notification period, the taxpayer has concluded that it has provided HMRC with sufficient information to determine whether to issue a preliminary notice and that HMRC has examined that information.

Practical experience of when notification is required

Typical transactions and industries that we have analysed in the past 12 months and that may require notification include:

banks and insurance;

hedge funds;

leasing; and

other structures that have (historically) included the existence of a low tax jurisdiction.

In addition, the following (not so obvious) transactions have also required a review and notification in some isolated cases:

wholly UK based structures with trapped losses; and

entities not operating in low tax jurisdictions but operating under favourable tax regimes (e.g. tonnage tax, tax holidays, real estate investment trusts).

Note that in most of the above cases, there was a strong commercial rationale behind the transactions, which permitted a ‘no notification’ position to be adopted. However, this did require financial economic analysis to support the fact that there was a contribution to economic value that outweighed any incidental tax benefit, thereby supporting both the substance of the transaction and the fact that it was not designed to convey a tax benefit.

Proving economic substance has also been assisted by revised OECD transfer pricing guidelines relating to risk. These depart from the notion that substance requires bodies on the ground (an archaic concept for the industries listed above) in a welcome change to the OECD guidance (see figure below).

We have also had some experience of what ‘sufficient information’ means in this context. It is clear that groups that are under existing advance pricing agreements, and/or that have informal agreements with HMRC in relation to transfer pricing, have still had to enter into a new dialogue with HMRC to confirm this. (In the majority of cases that have hit my desk, this has been a straightforward process: advance pricing agreements or informal agreements are rarely sought if there is not a strong commercial fact pattern in place.) Groups that are still unsure could consider a discussion with HMRC through the risk assessment channels in the next week or so to mitigate any potential tax-geared penalties at a later date. A transparent discussion may require an allocation of resources; however, this may be more efficient in the long term when one considers a potential challenge from HMRC and also financial audit fees at a later date to backtrack and resolve an uncertain position.