Immediately following the Scottish rate resolution on 20 February 2018, HMRC released a newsletter (bit.ly/2FN3WSy) explaining how it intends to operate tax relief at source (RAS) pension arrangements, to interact with the new Scottish tax rates and bands.

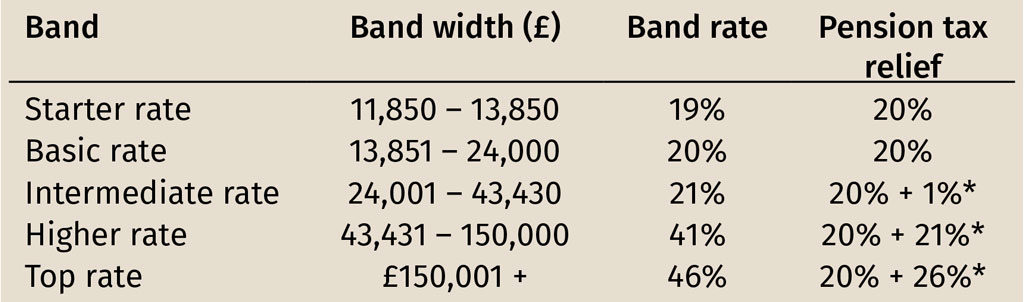

From 6 April 2018, Scottish taxpayers will pay tax in accordance with five income bands, as opposed to three in the rest of the UK. The rates and bands are set out in the table below, and the pension tax relief.

(The table assumes that a personal allowance of £11,850 can be claimed up to the income limit of £100,000, whereupon it is reduced by £1 for every £2 earned over that limit.)

*HMRC has noted that the taxpayer can claim the additional tax relief through self-assessment or by contacting HMRC if they are not a self-assessment taxpayer. There is no need to register for self-assessment just to claim additional tax relief.

At ICAS, we have concerns that unless taxpayers are in the self-assessment regime, they may miss out on their full entitlement to tax relief. How realistic is it to expect that HMRC can effectively ensure that all Scottish taxpayers (who they have had difficulties identifying in the past) who are not within the SA regime (and are thus unlikely to have much knowledge of RAS arrangements and pensions) know they need to contact HMRC?

A number of anomalies were thrown up by the introduction of new rates and bands, including gift aid, marriage allowance and pensions tax relief for RAS pension scheme members – the most prevalent of these being the pensions tax relief mechanism.

What do pension providers need to do?

Pension providers should continue to claim 20% tax relief on any RAS pension payments which are made by starter rate taxpayer scheme members. We understand that the Scottish government is funding the cost of the 1% difference, as HMRC will not be recovering the 1% difference.

A note about net pay arrangements

Employees with net pay arrangements are eligible for the same relief as those in registered and stakeholder RAS schemes. However, the difference is that under a net pay arrangement, the correct amount of tax relief is automatically applied in all cases and thus, there is no need to take any further action.

Some items not covered in the newsletter

Finally, a few points were not addressed in the HMRC newsletter. I assume they will be covered in later releases. For example, it is not yet clear whether HMRC will adjust tax codes or make reimbursements directly to eligible taxpayers; it is not clear precisely what information HMRC requires those RAS members who are not in self-assessment to send in; and it is not clear how any additional tax relief might find its way to funding the pension scheme of affected individuals.

Last but not least, giving tax relief at the right rate for pensions illustrates the operational difficulties with five tax rates imposed on a three-rate system. It remains to be seen how, or if, this will be addressed in the long run and whether administrative ease or purity of policy will be of greatest importance.