The big question ahead of this Budget was how the chancellor would pay for the large increase in NHS spending announced by the prime minister back in June. Further spending cuts in areas other than health seemed to have been ruled out by the prime minister’s later pledge to ‘end austerity’, so it looked as if some combination of higher taxes and higher borrowing would be needed.

In fact, the chancellor has been able to avoid significant net tax increases – and even cut some taxes in the short term through increased personal allowances and a freeze on fuel and some alcohol duties – while also keeping projected public borrowing more or less the same in the medium term as the OBR forecast in March. There will be some tax increases in later years, notably on large digital businesses and by tightening up rules on people who work through their own company, but no large broad-based tax increase of the kind that Gordon Brown, for example, introduced to help to pay for significant NHS spending increases in his 2002 Budget.

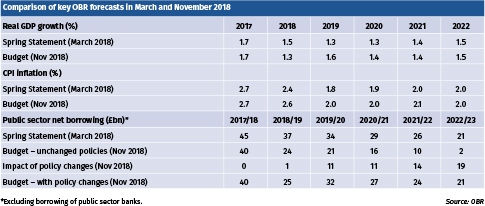

The chancellor was able to pull off this trick because the OBR handed him an unexpectedly large fiscal windfall by projecting that tax revenues in 2022/23 would be around £14bn higher than it forecast back in March, despite broadly unchanged GDP growth and inflation forecasts. Added to lower projected debt interest and some other smaller forecasting changes, the public finances in 2022/23 are now looking around £20bn better than in March, based on unchanged tax and spending policies (see table).

Had the chancellor not used this fiscal windfall to fund higher NHS spending, he could have projected a broadly balanced budget by 2022/23, rather than a £21bn deficit in that year. However, guided by the prime minister, he has favoured easing austerity over balancing the budget, while still hitting his key medium term fiscal target of reducing the structural budget deficit to below 2% of GDP with some comfort.

The OBR expects UK economic growth to remain modest by historical standards at 1.3% this year and an average of just 1.5% per annum over the next five years. This is a relatively cautious forecast, somewhat lower than that of the Bank of England and most other forecasters, though such caution may be sensible for fiscal planning purposes given the current uncertainties around Brexit.

If and when a Brexit deal with the EU is agreed, the OBR may revise up its growth forecasts slightly. We would not expect too much of a ‘deal dividend’ from this source, however, given that modest projected UK growth also reflects underlying problems related to slow productivity growth that were evident well before Brexit and indeed have been common to many other advanced economies in the period since the global financial crisis.

In addition to the extra money for the NHS, the chancellor also allocated an additional £3bn a year by 2022/23 to planned day-to-day spending by other departments, relative to indicative figures published in March.

This is just enough to keep real day-to-day spending by departments other than health broadly constant in real terms over the next spending review period rather than declining, which could meet a minimal definition of ending austerity. We will have to wait until later next year to see the full details of the spending review. At that point, some departments and local authorities may yet face further real cuts, given that areas like defence and overseas aid have been earmarked to receive real spending increases. So austerity is being eased, but arguably not yet ended for all parts of government.