A sweet and sour Budget, writes Chris Sanger (EY).

By the time a chancellor delivers his eighth Budget, he might be forgiven for hoping that things would start to get easier. However, against a background of deepening global uncertainty, and some political sensitivities at home, George Osborne had his work cut out maintaining his credentials as a tax cutting, reforming chancellor. In the end, he just about pulled it off, with some further steps down his reform path, a few robbings of Peter to pay Paul, and a resetting of the horizon for his ambitions towards the next generation.

What kind of Budget was this?

The chancellor fought hard to stick to his principles, but needed some nifty footwork and a few innovations to pull it off. He was able to continue his Long March to reduce the headline corporation tax rate, raise personal allowances and income tax thresholds, and increase incentives to save. He was even able to pursue a couple of items from his longer-term wish list: reducing the CGT rate (at least for some assets); and cutting business rates for small businesses. However, to pull this off he had to raid big business with a combination of changes to the corporation tax rules (driven by the base erosion and profit shifting (BEPS) initiative in the G20/OECD) and to corral a series of measures under the ‘avoidance and evasion’ label.

Beyond the number crunching, we also saw some interesting developments in terms of specific levies: the introduction of a sugary drink levy (or the ‘soft drinks industry levy’ as it’s officially called) will result in proceeds going to support of school sport; and hypothecation of the 0.5 percentage point increase in insurance premium tax going to flood defences.

What was in it for business?

Building on the successful innovation of the 2010 Corporate tax road map, the Budget launched its 2016 version, the Business tax road map, setting out the government’s ambition up to 2020. This approach is structured around three broad goals:

reducing tax to drive growth;

modernising the UK system in line with international best practice; and

levelling the playing field so that multinationals ‘pay their fair share’.

As well as setting out the direction of the government’s business tax ambitions for the rest of the decade, the new road map launches a range of specific tax measures. Much as this is welcome, the road map was clearly missing a few pages, particularly when compared to the hints being given just a week earlier. One hopes that these are still to come, rather than forgotten.

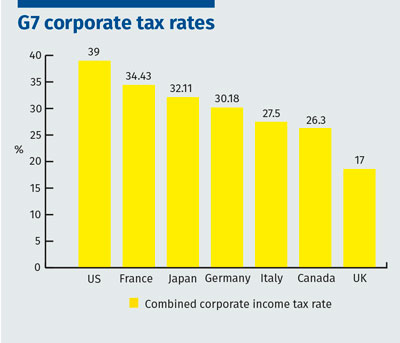

Seasoned Budget observers should by now have learned to expect the unexpected on corporation tax. Once again, the chancellor delivered a mild surprise by announcing a further cut (this time to 17% by 2020, giving the UK by far the lowest headline rate in the G7).

He balanced this out with measures targeted on supporting small business. Where many called for fundamental reform of the business rates system, the chancellor has opted for a more targeted approach of permanently doubling small business rate relief (to 100%), increasing the threshold for the standard rates multiplier (to £51,000) and moving indexation form RPI to CPI. This helps small businesses in particular but maintains the pain for their larger competitors, especially retailers and manufacturers.

In addition, the Budget ushers in reduced rates of CGT, with the higher rate moving from 28% to 20%; and the basic rate falling from 18% to 10%, but not for the increasingly put-upon buy-to-let landlords.

So where was the pain?

While these benefits will be shared across the economy, it is large businesses that will foot the bill. The biggest hit for larger businesses comes from the chancellor’s determination that the UK should remain at the forefront of the international initiative on BEPS, as well as other changes to the CT regime.

These measures include:

a new cap on interest relief (set at 30% of taxable earnings, and subject to group ratio test, a de minimis limit and a public benefit exemption);

new rules on withholding tax on royalty payments;

an extension of the rules on hybrid mismatches; and

legislation to counter the use of offshore structures to avoid tax on UK property developments.

Extending the restrictions on the use of losses by banks to all UK companies was somewhat surprising, given the chancellor had previously implied that he had only taken that step with the banks because they had benefited from government support during the financial crisis. Such logic seems to apply no longer, although the restrictions were further tightened for the banks.

Taken together, these measures will see larger business contribute a whopping £1.5bn a year to the chancellor’s take from 2017 onwards. On top of the BEPS measures, the chancellor announced a modernisation of SDLT for non-residential properties which also raised the burden by £0.5bn per annum.

Anything for the new economy?

In addition to the reductions to CGT, the chancellor has sought to boost enterprise by measures such as the abolition of class 2 NICs for the self-employed, and by introducing new allowances (£1,000 each on trading income and property income) to support the sharing economy.

What about personal tax?

The Budget continued to deliver the tax cuts that George Osborne has always promised. This time around, the cuts come in the form of an increased personal allowance (up to £11,500 from 2017) and an increase in the higher rate threshold (up to £45,000 from 2017).

On the pensions front, having rowed back from a wholesale cash grab on pension tax relief, the main measure is the launch of lifetime ISAs, designed to encourage young people to save for pensions in a vehicle which doesn’t look like a pension. From April 2017, the lifetime ISA will enable adults under 40 to save £4,000 a year (and receive a 25% top up from the government). Time will tell how risky it is to allow people to save for a pension with an ISA which can be used for other purposes, such as buying a house.

What about duties?

Osborne’s romance with beer continued to flourish, with a further duty freeze, while the continued freeze on fuel duty can be expected to raise a cheer from motorists and small businesses alike.

Any word on simplification?

While the chancellor said in his speech that he remains committed to the tax simplification project, it is notable that today’s Red Book did not engage with the issue, beyond claiming the uprating of the VAT threshold as a simplification measure and signalling further future action by the Office of Tax Simplification. In contrast, there is a case to be made that this Budget, like its predecessor in Summer 2015, actually adds to the complication of the tax system through the introduction of additional allowances. (This time, the allowances are for investment in the shared economy; in the Summer Budget, they were for dividends and personal saving.)

Any innovation?

In a world where the triple lock has disconnected the main tax raising levers, the chancellor is going to have to find new and interesting ways of raising tax, but which do not too overtly run counter to his overall stance on the joys of lower taxes. Innovations in this budget include a sugar levy and a minimum excise tax to shore up the tax take on tobacco.

Another innovation is the emergence of a new category of ‘imbalances’, alongside ‘evasion’ and ‘avoidance’. Imbalances under this definition potentially includes the treatment of free plays in remote gambling, carried interest for asset managers, employee shareholder schemes, salary sacrifice, loans to participators and pay-offs. While there is no suggestion that the current practice amounts to either evasion or avoidance, the new notion of imbalances provides the government with a pretext for action. One to watch.

So was this a giveaway or a cash grab?

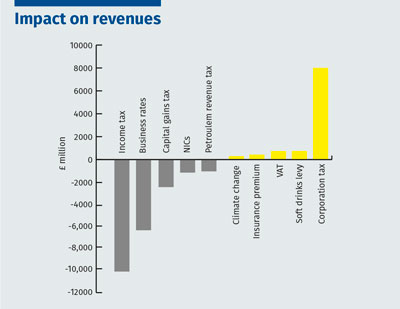

That depends on who you are. Overall, the balance was one where individual and small businesses benefited from the chancellor’s largesse, while big business footed the bill, but nevertheless received some good news. As the table below shows, the overall profile of the Budget takes us on a bumpy ride of peaks and troughs over the five year period, as this most political of chancellors uses his policy decisions to meet his long term targets.

And perhaps the most striking feature is the extent to which a Budget which reduces the corporation tax rate yet again still sees business tax footing the bill for tax cuts elsewhere.

A sweet and sour Budget, writes Chris Sanger (EY).

By the time a chancellor delivers his eighth Budget, he might be forgiven for hoping that things would start to get easier. However, against a background of deepening global uncertainty, and some political sensitivities at home, George Osborne had his work cut out maintaining his credentials as a tax cutting, reforming chancellor. In the end, he just about pulled it off, with some further steps down his reform path, a few robbings of Peter to pay Paul, and a resetting of the horizon for his ambitions towards the next generation.

What kind of Budget was this?

The chancellor fought hard to stick to his principles, but needed some nifty footwork and a few innovations to pull it off. He was able to continue his Long March to reduce the headline corporation tax rate, raise personal allowances and income tax thresholds, and increase incentives to save. He was even able to pursue a couple of items from his longer-term wish list: reducing the CGT rate (at least for some assets); and cutting business rates for small businesses. However, to pull this off he had to raid big business with a combination of changes to the corporation tax rules (driven by the base erosion and profit shifting (BEPS) initiative in the G20/OECD) and to corral a series of measures under the ‘avoidance and evasion’ label.

Beyond the number crunching, we also saw some interesting developments in terms of specific levies: the introduction of a sugary drink levy (or the ‘soft drinks industry levy’ as it’s officially called) will result in proceeds going to support of school sport; and hypothecation of the 0.5 percentage point increase in insurance premium tax going to flood defences.

What was in it for business?

Building on the successful innovation of the 2010 Corporate tax road map, the Budget launched its 2016 version, the Business tax road map, setting out the government’s ambition up to 2020. This approach is structured around three broad goals:

reducing tax to drive growth;

modernising the UK system in line with international best practice; and

levelling the playing field so that multinationals ‘pay their fair share’.

As well as setting out the direction of the government’s business tax ambitions for the rest of the decade, the new road map launches a range of specific tax measures. Much as this is welcome, the road map was clearly missing a few pages, particularly when compared to the hints being given just a week earlier. One hopes that these are still to come, rather than forgotten.

Seasoned Budget observers should by now have learned to expect the unexpected on corporation tax. Once again, the chancellor delivered a mild surprise by announcing a further cut (this time to 17% by 2020, giving the UK by far the lowest headline rate in the G7).

He balanced this out with measures targeted on supporting small business. Where many called for fundamental reform of the business rates system, the chancellor has opted for a more targeted approach of permanently doubling small business rate relief (to 100%), increasing the threshold for the standard rates multiplier (to £51,000) and moving indexation form RPI to CPI. This helps small businesses in particular but maintains the pain for their larger competitors, especially retailers and manufacturers.

In addition, the Budget ushers in reduced rates of CGT, with the higher rate moving from 28% to 20%; and the basic rate falling from 18% to 10%, but not for the increasingly put-upon buy-to-let landlords.

So where was the pain?

While these benefits will be shared across the economy, it is large businesses that will foot the bill. The biggest hit for larger businesses comes from the chancellor’s determination that the UK should remain at the forefront of the international initiative on BEPS, as well as other changes to the CT regime.

These measures include:

a new cap on interest relief (set at 30% of taxable earnings, and subject to group ratio test, a de minimis limit and a public benefit exemption);

new rules on withholding tax on royalty payments;

an extension of the rules on hybrid mismatches; and

legislation to counter the use of offshore structures to avoid tax on UK property developments.

Extending the restrictions on the use of losses by banks to all UK companies was somewhat surprising, given the chancellor had previously implied that he had only taken that step with the banks because they had benefited from government support during the financial crisis. Such logic seems to apply no longer, although the restrictions were further tightened for the banks.

Taken together, these measures will see larger business contribute a whopping £1.5bn a year to the chancellor’s take from 2017 onwards. On top of the BEPS measures, the chancellor announced a modernisation of SDLT for non-residential properties which also raised the burden by £0.5bn per annum.

Anything for the new economy?

In addition to the reductions to CGT, the chancellor has sought to boost enterprise by measures such as the abolition of class 2 NICs for the self-employed, and by introducing new allowances (£1,000 each on trading income and property income) to support the sharing economy.

What about personal tax?

The Budget continued to deliver the tax cuts that George Osborne has always promised. This time around, the cuts come in the form of an increased personal allowance (up to £11,500 from 2017) and an increase in the higher rate threshold (up to £45,000 from 2017).

On the pensions front, having rowed back from a wholesale cash grab on pension tax relief, the main measure is the launch of lifetime ISAs, designed to encourage young people to save for pensions in a vehicle which doesn’t look like a pension. From April 2017, the lifetime ISA will enable adults under 40 to save £4,000 a year (and receive a 25% top up from the government). Time will tell how risky it is to allow people to save for a pension with an ISA which can be used for other purposes, such as buying a house.

What about duties?

Osborne’s romance with beer continued to flourish, with a further duty freeze, while the continued freeze on fuel duty can be expected to raise a cheer from motorists and small businesses alike.

Any word on simplification?

While the chancellor said in his speech that he remains committed to the tax simplification project, it is notable that today’s Red Book did not engage with the issue, beyond claiming the uprating of the VAT threshold as a simplification measure and signalling further future action by the Office of Tax Simplification. In contrast, there is a case to be made that this Budget, like its predecessor in Summer 2015, actually adds to the complication of the tax system through the introduction of additional allowances. (This time, the allowances are for investment in the shared economy; in the Summer Budget, they were for dividends and personal saving.)

Any innovation?

In a world where the triple lock has disconnected the main tax raising levers, the chancellor is going to have to find new and interesting ways of raising tax, but which do not too overtly run counter to his overall stance on the joys of lower taxes. Innovations in this budget include a sugar levy and a minimum excise tax to shore up the tax take on tobacco.

Another innovation is the emergence of a new category of ‘imbalances’, alongside ‘evasion’ and ‘avoidance’. Imbalances under this definition potentially includes the treatment of free plays in remote gambling, carried interest for asset managers, employee shareholder schemes, salary sacrifice, loans to participators and pay-offs. While there is no suggestion that the current practice amounts to either evasion or avoidance, the new notion of imbalances provides the government with a pretext for action. One to watch.

So was this a giveaway or a cash grab?

That depends on who you are. Overall, the balance was one where individual and small businesses benefited from the chancellor’s largesse, while big business footed the bill, but nevertheless received some good news. As the table below shows, the overall profile of the Budget takes us on a bumpy ride of peaks and troughs over the five year period, as this most political of chancellors uses his policy decisions to meet his long term targets.

And perhaps the most striking feature is the extent to which a Budget which reduces the corporation tax rate yet again still sees business tax footing the bill for tax cuts elsewhere.