UK economic growth has slowed this year and this more sluggish performance is now projected to continue for some years to come, as productivity growth remains disappointing. This has worsened the medium term public finance outlook and reduced the wriggle room available to the chancellor. He therefore had to walk a narrow tightrope in his Budget between maintaining a downward path for the budget deficit and responding to widespread pressures for an easing of austerity.

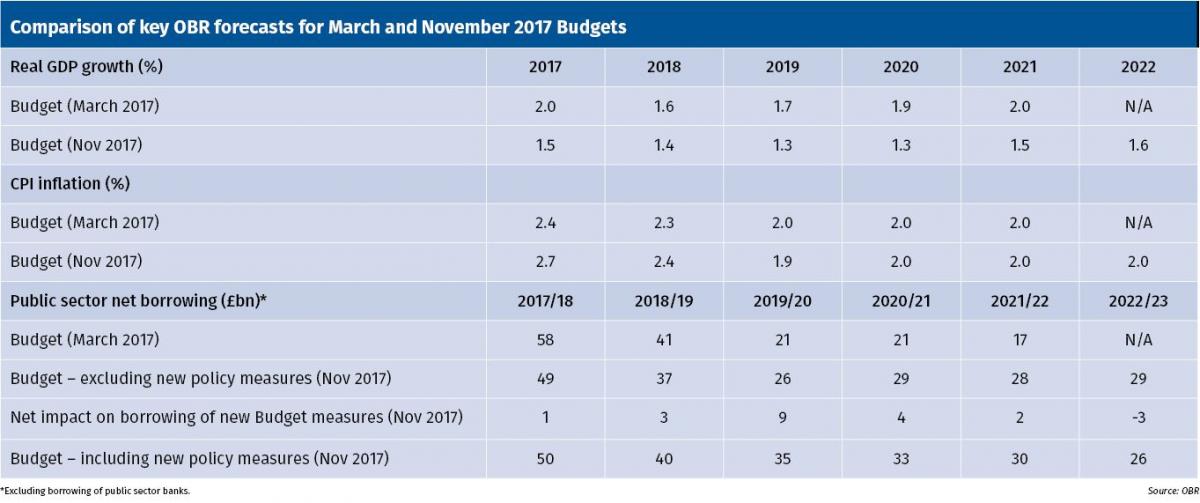

The Office for Budget Responsibility (OBR) revised down its 2017 GDP growth forecast from 2% to 1.5%, as higher inflation has bitten into consumer spending power and Brexit-related uncertainty has dampened business investment growth. Despite this slower growth, the OBR also revised down its public borrowing estimate for 2017/18 from around £58bn to only around £50bn, given better than expected public finance data so far this year (see table below).

However, the OBR judged that this short-term borrowing undershoot is unlikely to persist. Looking further ahead, the OBR has revised down its GDP growth projections significantly for each of the next four years, due to slower than previously expected productivity growth. By 2021, the UK economy is now expected to be more than 2% smaller than forecast in March; and this gap will only grow in later years if productivity growth remains subdued.

Slower economic growth translates to slower projected tax revenue growth and so to a higher budget deficit in the medium term – around £28bn in 2021/22 on unchanged policies as opposed to the £17bn OBR forecast back in March. This is despite a £4bn public borrowing reduction in 2021/22, due to housing associations being reclassified from the public to the private sector following recent regulatory changes.

The chancellor is still projected to meet his medium term target of getting the structural budget deficit below 2% of GDP in 2020/21 with some margin for error, but his headroom has shrunk since March from around £26bn to around £15bn now.

If prudence was his only concern, the chancellor might have responded to less favourable OBR forecasts by tightening fiscal policy over the next few years. But the chancellor also recognised that he needed to respond to political pressures to ease austerity and start to address fundamental economic challenges relating to housing and productivity.

The Budget therefore eased tax and spending policy significantly in the short term, increasing borrowing in 2019/20 by around £9bn. There were giveaways on housing and infrastructure, health, freezing fuel and alcohol duties and business rate indexation, as well as an extra £3bn of spending on Brexit preparations over the next two years. Aside from housing and infrastructure, however, most of these measures were only temporary and money will be clawed back in the medium term through various tax avoidance measures and other policy changes.

The chancellor will be hoping that UK growth is not as sluggish over the next few years as the OBR now forecasts, in which case he could have more room for manoeuvre in future Budgets. But it is far from guaranteed that the Brexit negotiation process will go smoothly, so the chancellor was prudent to adopt a relatively cautious approach for now, while doing what he could to address concerns around housing, health and longer term productivity growth.