What do the May 2021 Scottish election results mean for Scottish tax policy? Most of the media focus has inevitably been on covid recovery and the Scottish independence debate, so very little airtime has been devoted to the manifesto pledges of each of the different political parties. In this article, we examine the detail of Scottish taxation policy for the next parliamentary term.

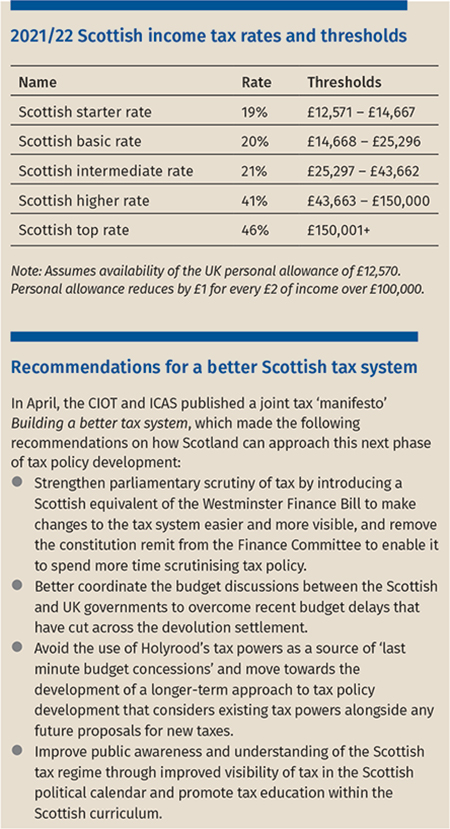

The process for devolving taxes in Scotland started some 20 plus years ago. Yet it is only in the last five years when that process produced legislation through which Scotland has differentiated itself from the rest of the UK. This is particularly so for income tax when, in 2018, Scotland introduced five rates and bands of Scottish income tax. Because of the partially devolved nature of the tax, not only do Scottish taxpayers with more than one source of income have to calculate their income tax liability using two computations – a UK rates and bands one for savings and dividends income, and a Scottish rates and bands one for the rest – but they also face added complexities in relation to certain tax reliefs, such as on pension contributions.

The limited nature of Scotland’s tax raising powers has at least provided some stability for taxpayers and for the Scottish government too, as it has facilitated a gradual transition from a spending budget to a revenue raising and spending budget. Scotland has been able to dip its toe in the water of revenue raising from national taxes and configure its own legislative and parliamentary processes as it goes along.

During this process, the Scottish government has established a Tax Directorate, which has proved a very positive move as it enables officials to consider policy and legislation in more detail and liaise with stakeholders (including ICAS and the CIOT) on a regular basis.

But there are frustrations with the constraints on Scotland’s limited tax powers. The new national Scottish taxes must be agreed by the UK Parliament, and the expectation that up to 50% of Scottish taxes would be devolved by 2021 has been stymied by the difficulties in developing a suitable methodology for the ‘assignment’ of Scottish VAT receipts to Scotland (originally provided for in Scotland Act 2016). VAT assignment appears to have been kicked into the long grass for now. It may not reappear until the fiscal framework review, which is due to take place over the course of 2021, has been completed as part of the Scottish government’s medium term financial strategy.

So far, only three devolved taxes have gone live:

Legislation for a fully devolved air departure tax has been passed (the Air Departure Tax (Scotland) Act 2017), but the tax is still not live because of ongoing difficulties with state aid and the Highlands and Islands exemption. It is likely that the SNP and the Scottish Greens may formulate a form of hybrid regime that seeks to complement the environmental agenda – perhaps, as the Greens suggest, by increasing the taxes on flights the more frequently you fly. Consultation is expected on a fully devolved tax to replace the UK aggregates levy on the commercial exploitation of aggregate in Scotland.

Two new taxes were proposed in 2019 by the Green Party during negotiations to pass the Scottish Budget for 2019/20: the workplace parking levy and transient visitor levy (‘tourist tax’). These taxes cannot be raised at national level due to the constraints on powers mentioned above: they are intended to be local taxes raised by those local authorities who wish to implement them. Progress has stalled due to covid, and it remains to be seen whether they will be picked up again by new Parliament after the summer break.

Other mainstream taxes, such as capital gains tax and corporation tax, remain applicable across the UK, are based on UK legislation in the Taxes Acts, and are collected and administered by HMRC. National insurance contributions also continue to be legislated for by the UK Parliament and collected by HMRC on a UK-wide basis.

Council tax and non-domestic rates continue to be raised and administered by local authorities in Scotland.

In the May election, the SNP failed to win an outright majority of 65 by one seat. The Scottish Conservatives came second with 31 seats. Scottish Labour won 22 seats. Although the Greens were only fourth with eight seats, their importance cannot be underestimated in terms of Scotland’s potential future – because they believe that a greener future for Scotland is enhanced by it being independent of the UK. Therefore, as has been the case in the past, the SNP is likely to do deals with the Greens to get their motions through Parliament.

In light of the above, we concentrate below on the tax manifestos of the above four parties on two key areas: SIT and property taxation.

Whilst the SNP has pledged to freeze SIT rates for the next five years, in a bid to aid stability post-pandemic, the bands will increase by ‘a maximum of inflation’. This could mean that they don’t increase at all: time will tell. Meanwhile, the UK government has pledged not to increase the UK personal allowance or the higher rate threshold. There may therefore be some further divergence in bandings between Scotland and the rest of the UK in the short term. The main consequence will be the persistence of the spike in joint marginal income tax and NICs rates that affects Scottish PAYE taxpayers in the so-called ‘middle income earnings band’ of £43,663 to £50,270. These taxpayers not only pay SIT of 41%, but also NICs of 12%, resulting in a marginal tax rate of 53%. Their counterparts in the rest of the UK pay a 32% marginal rate on that same income band.

It’s unlikely the SNP stance will be a dealbreaker for the Greens: their manifesto pledge was merely to support a ‘more progressive approach’ and it gave no underlying detail.

Both Labour and Conservatives erred more on the side of growing the economy to increase the tax base rather than tinkering too much with tax rates and bands. Labour would focus on those earning over £100,000 per annum, whilst the Conservatives would retain the 19% starter rate and lower the taxes to be in line with the rest of the UK by the end of the term.

The SNP has pledged to retain the status quo as far as LBTT goes over the duration of the next Parliament, and has committed to review the additional dwelling supplement, which has caused many issues since its introduction in 2016. The SNP’s efforts to maintain a status quo may be influenced by the Greens, however, because the latter pledged to support housing cooperatives through targeted relief from LBTT, as well as to undertake a review on vacant and derelict land, which partially ties into the objectives of the Scottish Land Commission.

During 2020/21, the Scottish government raised the LBTT threshold to £250,000 as a temporary measure to act as an easement for purchasers during covid, and the Scottish Conservatives would like this to remain in place – albeit it was withdrawn in March of this year. They consider that this would attract more investors to the Scottish property market as a concession to the more ‘progressive’ SIT rates and bands which some commentators have said could make Scotland less competitive. A review of the additional dwelling supplement will also receive their support. Surprisingly, the Scottish Labour Party had no proposals for LBTT.

In terms of council tax, the SNP has committed to making the system fairer, without going into any detail. The SNP will come under some pressure from the Greens to reform the tax. The Greens want a modernised residential property tax that will be based on up to date property values.

Scotland has started to convene citizens assemblies on socio-economic matters, and both the SNP and the Greens are keen to hold taxation-specific events in future.

The prospect of an independence referendum should now be on the agenda for all tax advisers and business investors, thanks to this last set of election results. It will be important to maintain a watching brief on the developments over the next few years. It is likely that not much will happen in terms of an independence referendum until clear evidence exists that the pandemic no longer presents a real and present threat in Scotland. However, after that, it is likely the wheels will be set in motion in earnest.

It will be necessary for taxpayers, investors and advisers to be up to speed on the proposals being tabled for an independent Scotland, due to the high numbers of Scots who voted for parties with an independence agenda. The likelihood of a focus on more progressive taxes including wealth, property, land distribution and inheritance, as well as foreign ownership taxes could be part of any future roadmap of an independent Scotland.

On the face of it, the 6 May election didn’t change much, but the implications will be profound should the election pave the way for Scottish independence. In any event, it is likely that there will be a fair bit of tinkering in tax policy in the coming years. The immediate focus of advisers needs to be on the outcome of the additional dwelling supplement review. In the medium term, an eye should be kept on the introduction of new taxes, such as air departure tax and the transient visitor levy.

ICAS has recently updated the ICAS Guide to Scottish Taxes which contains details of all the current positions for the full range of Scottish Taxes.