Since the recession there has been a rapid rise in the number of individuals operating through self-employment or company owner-management. These groups are taxed substantially less heavily than employees despite receiving very similar state benefits. This creates a tax system that is complex, inefficient and unfair. In Budget 2017, the chancellor tried to take a small step towards a better tax system by increasing self-employed NICs. He failed. The best thing we can do now is unite around a long run vision for how we should tax different ways of working and start designing a pathway for getting there.

It has become commonplace to state that the labour market is fundamentally changing and that secure employment positions are being replaced with independent contract relationships that are more flexible but that also come with intermittent and less secure income streams and fewer rights. But to what extent is this true?

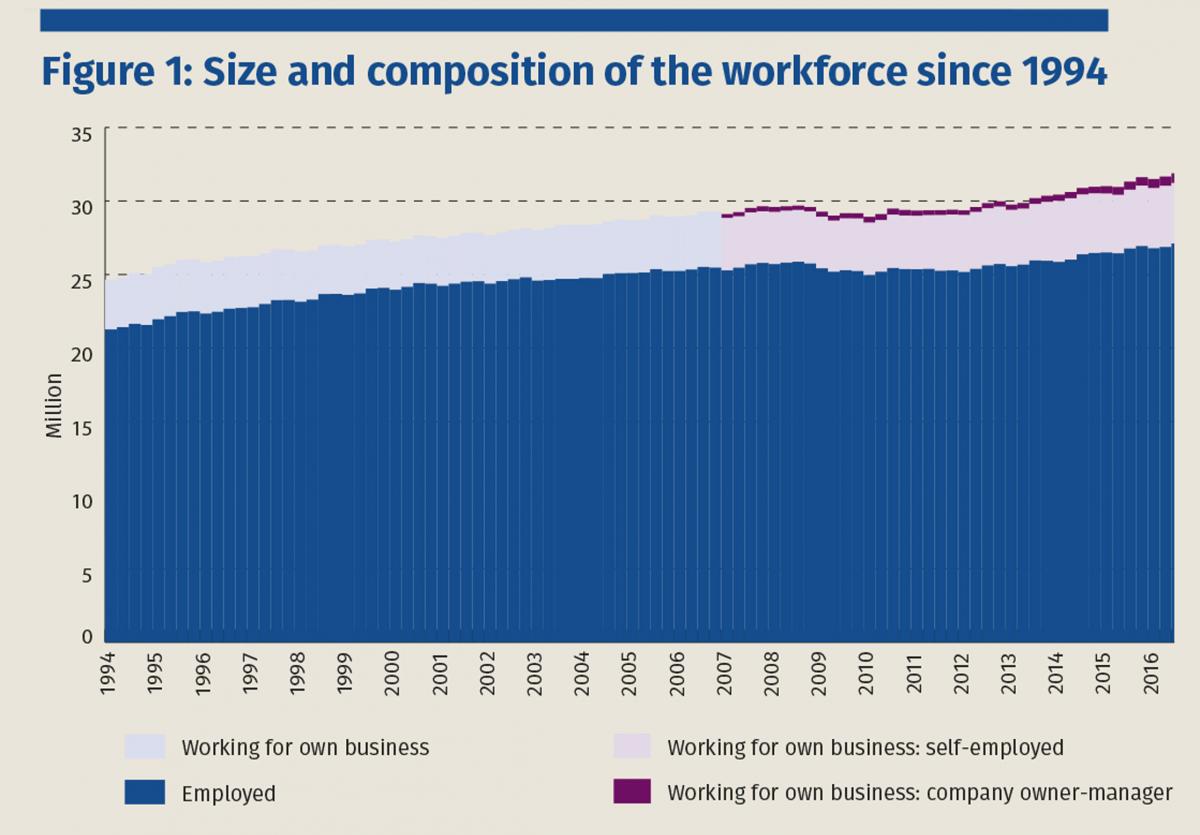

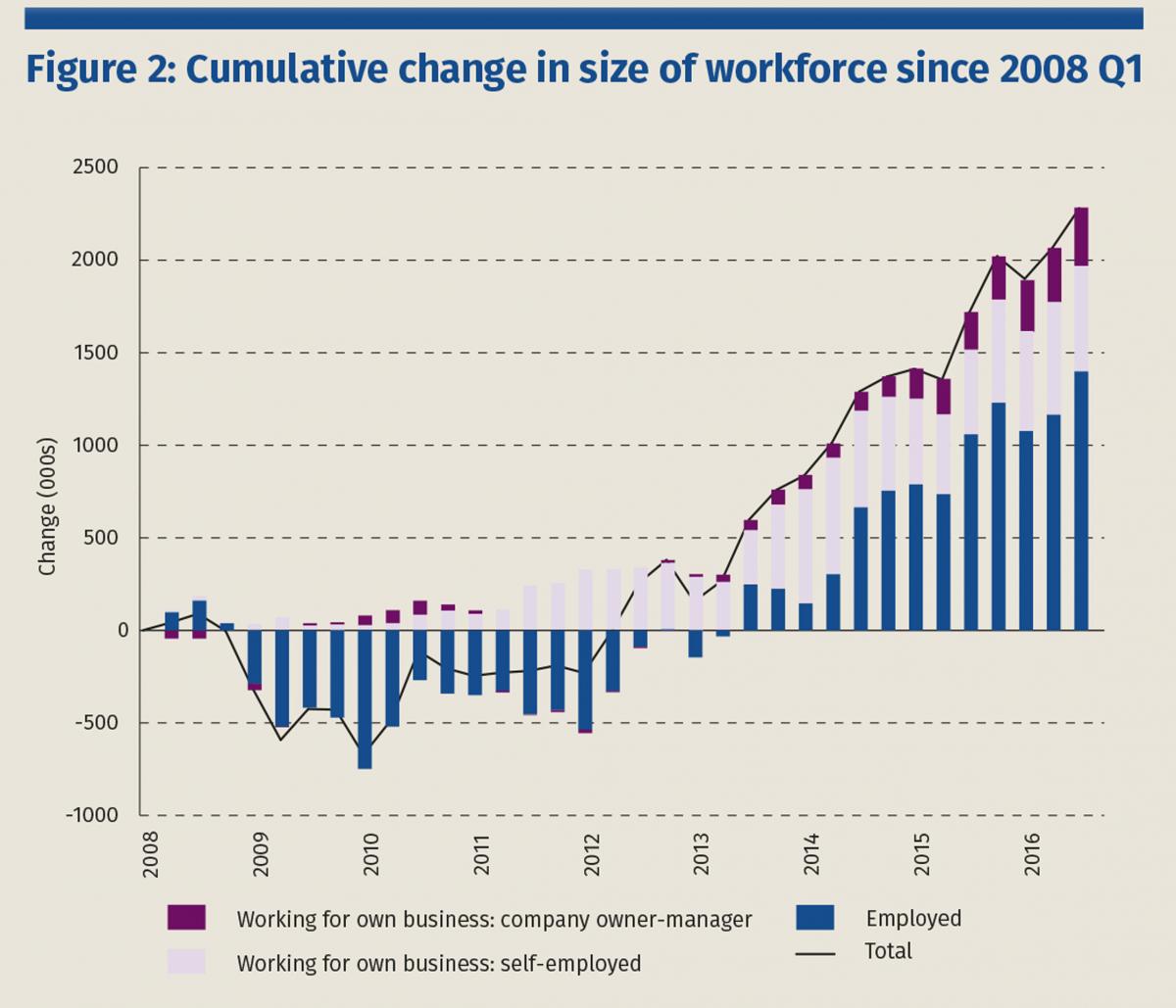

The majority (85%) of the UK’s 31.1m strong workforce is still made up of employees, 94% of whom are in permanent positions. Figure 1 (below) shows the changing composition of the workforce and from that you’d be forgiven for wondering what all the recent fuss is about. But, zoom in, and we can see that the labour market has been changing. Figure 2 (below) shows that since 2008, 40% of the cumulative increase in the workforce (shown in the black line) has resulted from an increase in the number of individuals working for their own business. Of this 40% cumulative increase, just over one-third is attributable to an increase in company owner-managers and just under two-thirds to an increase in self-employment. This translates into a larger proportional increase in the company owner-manager population, which has almost doubled since 2008. This growth has been a significant part of the good news employment story that we’ve seen since the Great Recession and that has been the silver lining to depressingly weak productivity growth.

At first blush, these statistics chime with anecdotal evidence on the so-called ‘gig economy’. Many people, especially those in London, have become accustomed to taking Ubers, having their food ‘deliverooed’ and hiring taskers to help with their chores. Such jobs are undoubtedly part of the labour market changes. But are these new ways of working responsible for all of the recent movement away from employment? No one knows for sure, but the answer is almost certainly no.

Beyond the anecdotes, there is no clear definition of who is and isn’t working in the ‘gig economy’. Broadly, the term is used to capture those workers who operate independently (usually through self-employment), perform work that can be broken down into separate tasks (‘gigs’) and use a digital platform operated by a large company to match them to customers. It is really the digital platforms that distinguish such workers from previous generations of the self-employed – many of whom also undertook comparable ‘gigs’ and used platforms run by third parties. Assuming we could agree on a definition of the gig economy, our traditional sources of data (most notably the surveys collected by the Office for National Statistics) are not designed to capture the gig economy or many of the characteristics of different forms of employment. What we can say, though, is that the industries in which the growth in self-employment has been most prominent are not those most associated with the gig economy; it’s not all taxi drivers and delivery drivers. This suggests that there is a broader-based change in working patterns under way. New surveys point in the same direction. For example, a McKinsey survey found that 15% of ‘independent workers’ across Europe and the US have used a digital platform, suggesting that this way of working is important but not ubiquitous.

One interpretation of the recent changes is that entrepreneurial individuals are breaking away from their employers and exploiting the opportunities offered by new technologies. A less rosy interpretation is that individuals have been choosing self-employment (or company ownership) because they lack employment opportunities and/or have been pushed into self-employment by companies that are looking to avoid legal obligations such as the national minimum wage, statutory sick and holiday pay and immigration checks. In this case, rather than reflecting the road to freedom and creativity, the growth in self-employment more likely marks the start of a more precarious and stressful way of working. Anecdotal evidence, and some high profile court cases, suggests that at least some of the newly self-employed would prefer to be employees.

It should be surprising that the market seems to be favouring individuals working for their own business, rather than as employees of large companies. Companies exist precisely because it is usually more efficient for individuals to come together as part of a large company than to operate many small businesses with contractual relationships between them (there are economies of scale and scope). Part of the explanation is likely to lie in employment laws that effectively make employees more expensive for employers. But the tax system is also giving individuals a pretty big nudge towards working for their own business.

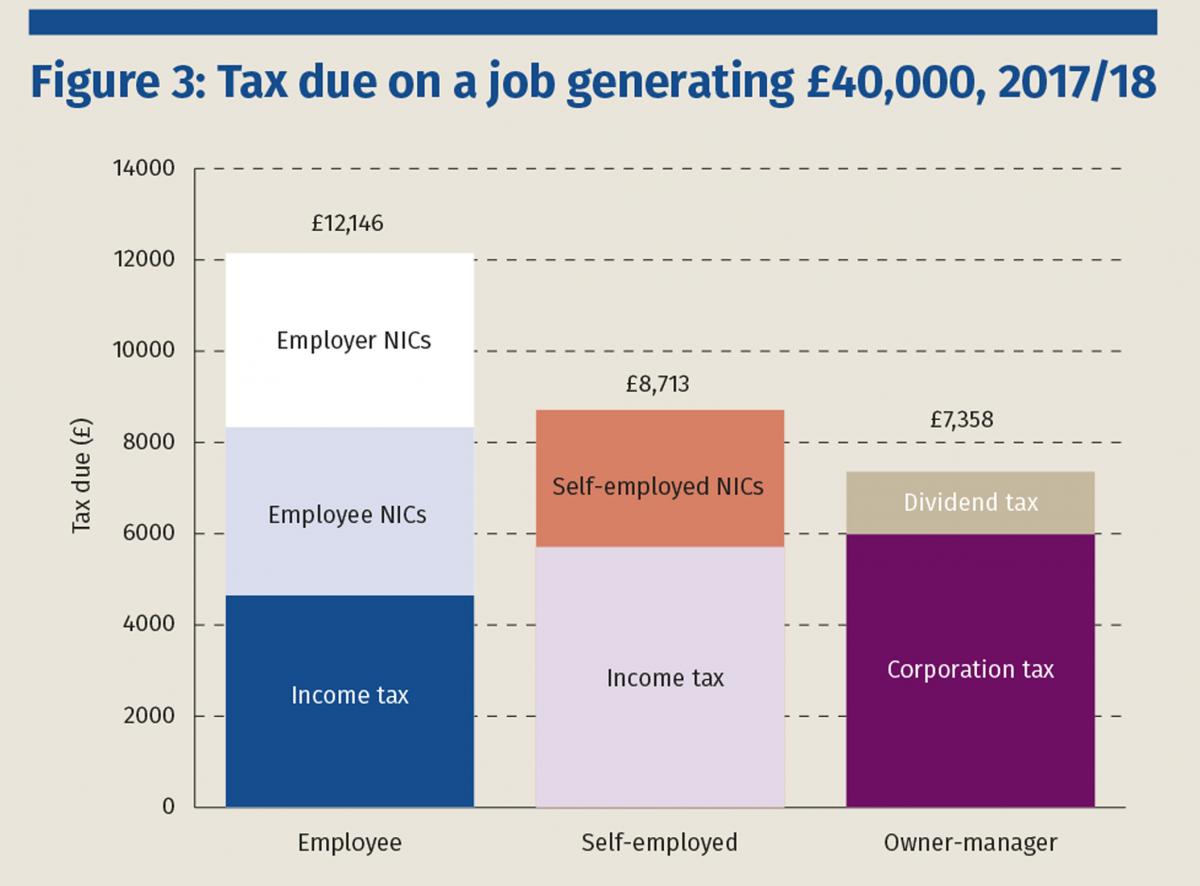

Thanks in part to Philip Hammond’s failed attempt to increase national insurance contributions (NICs) on the self-employed in Budget 2017, it is now common knowledge that self-employment income is taxed at substantially lower rates than employment income. But the scale of the difference can still come as a surprise. Figure 3 (below) demonstrates the tax differences for an example person generating £40,000 of income per year. The total tax liability will be £12,146 if the income is generated by an employee but just £8,713 – over £3,000 lower – if the income is earned through self-employment. That entire difference is driven by the fact that the self-employed are charged a lower rate of NICs and, most importantly, face no equivalent to employer NICs. Company owner-managers can get even lower tax rates than the self-employed because they can choose to take income out of their company in the form of (more lightly taxed) dividends rather than as wages. This entails paying corporation tax on business profits, and then paying income tax (but not NICs) on dividends at the personal level. For them, the example £40,000 job will attract tax of just £7,358. In this example, the employee faces a 30% average tax rate, compared with 22% for the self-employed person and 18% for the company owner-manager. The rate for owner-managers will fall as the corporate tax rate falls to 17% in 2020/21.

These figures will actually understate the tax advantages associated with self-employment or company owner-management. The self-employed generally have more scope to deduct work-related expenses from their income than employees do. And there are other (legal) ways to lower taxes, such as shifting income to a spouse by paying them a wage and/or making them a shareholder. Company owner-managers who can retain income in their businesses and later realise that income in the form of capital gains when the business is sold or dissolved can get some of the lowest rates. This is because under entrepreneurs’ relief, which many company owner-managers will qualify for, capital gains are taxed at just 10%.

The self-employed and company owner-managers also have greater opportunities to (legally) avoid or (illegally) evade taxes than employees. It’s hard to estimate precisely how much this costs the Exchequer in foregone revenues, but it’s non-trivial. Around 30% of self-employed tax returns are estimated to understate the amount of tax due, while this is true of just 12% of the remainder of self-assessment tax returns (which largely belong to higher- and additional-rate taxpayers). HMRC estimates that the self-employed account for £5bn of the £7bn uncollected ‘tax gap’ for self-assessment income tax, NICs and capital gains tax combined.

Finally, the VAT system adds one more cherry on this cake. Companies with a turnover below £83,000 are exempt from VAT. This can create a tax difference depending on whether activities are provided by a large company or many small companies (e.g. one taxi firm operating with employees is more likely to be subject to VAT than if the same number of journeys is provided by many independent taxi drivers). Battles look likely to rage over whether platform providing companies such as Uber should be legally obliged to collect VAT. But the incentives created by the VAT threshold extend beyond jobs that are conducted via platforms.

This is clearly a whistle-stop tour of the tax treatment of different ways of working. And it’s worth noting that there are some cases where the self-employed are disadvantaged relative to employees. For example, unlike employees and company owner managers, the self-employed cannot access NICs relief on pension contributions. The self-employed are also treated less generously by the benefits system than employees. But overall and in the vast majority of cases, there is a substantial tax advantage to earning income through your own business rather than through employment by somebody else’s business.

Of course, lower taxes don’t count as a free lunch if they are simply compensating for other disadvantages that the government attaches to different legal forms. However, this preferential treatment cannot be justified as compensation for reduced state benefit entitlements or lower employment rights.

Arguing that the self-employed should get lower tax rates to reflect reduced entitlement to some social security benefits is fine in principle, but the small differences in access to contribution based benefits cannot account for the large NICs difference. Unlike employees, the self-employed are not entitled to contribution-based jobseeker’s allowance or statutory parental benefits (although they do have access to maternity allowance, which makes the difference in treatment smaller than is often thought). A back of the envelope calculation suggests that the lack of these two benefits could justify substantially less than a 1 percentage point difference between the NICs rates of employees and the self-employed. Currently, the difference is almost 14 percentage points. We could have justified a larger difference if the self-employed still got lower pension entitlements. But since April 2016, employees and the self-employed have been accruing rights to the same single-tier pension. At the point of introduction, this was actually a substantial giveaway to the self-employed who will now get a higher pension despite having paid less NICs than equivalent employees and continuing to benefit from lower rates.

Arguing that the self-employed should get lower tax rates to reflect the lack of employment rights is an enticing sounding argument but is logically flawed. It is true that employment law bestows employees with a set of rights, such as holiday pay and sick pay, which self-employed people do not have. However, unlike higher state benefit entitlements, these employment rights are not a benefit given by the government to employees, but a benefit that the government requires employers to give to their employees. In so far as these rights make employment more attractive to the employee (relative to self-employment), they also make employment less attractive to the employer (relative to getting the work done by a self-employed contractor). Overall, the government is not favouring employment over self-employment in a way that might justify an offsetting tax differential; it is merely redistributing between the two parties within an employment relationship. Indeed, in a well-functioning labour market, we would expect an employee’s greater employment rights to be offset by lower earnings, making them (on average) no more likely to choose employment over self-employment than they would in the absence of these rights. This is good news. There are lots of really important issues around how to design employment rights to ensure that they are not too burdensome but that they offer protection to workers who lack market power. But our design of tax policy does not need to change based on what we chose to do with employment rights.

The complexity is easy to see. Giving such different tax treatment to different groups means we must devise and administer rules to distinguish the different legal forms. This imposes costs, including those that stem from having to divert officials, taxpayers, accountants and occasionally the courts from more productive activities. The distinctions inevitably open up possibilities for avoidance and evasion – further exacerbating the problems of unfairness, inefficiency and diverted resources.

The unfairness arises because similar individuals with similar earnings can face very different tax burdens. In fact, many of the problems created by the current tax system arise precisely because we have erected sharp boundaries into a spectrum of ways of working.

The inefficiency arises because the stark incentives created by the tax system clearly distort individuals’ choices. Our economy is less efficient because some people are induced to run their own businesses when, if incentives were not distorted by the tax system, they would rather be employed by others. Put more plainly, we would all be better off if some current business owners scrapped their low productivity business models and instead worked as an employee for a more successful business.

Taxes also impact economic efficiency by affecting how individuals choose to take their income. We recently saw a clear example of this. In July 2015, the government announced that the tax rate on dividends would increase by 7.5 percentage points in April 2016. This gave individuals an incentive and ample time to bring dividends payouts forward (to between July 2015 and April 2016) to avoid paying the higher rate expected later. Unsurprisingly, this is exactly what many people did. In fact, the extent of dividend forestalling was sufficiently large that it boosted tax revenues by £4bn in 2016/17. Revenues will now be lower in coming years. The estimated tax savings for individuals (and therefore the loss to government revenues) is £800m. Remarkably, over £100m of that saving went to just 100 individuals who, on average, withdrew £30m of dividends from their companies in response to the tax changes.

The problems associated with having such large tax differences across legal forms aren’t new. Economists, including those at the Institute for Fiscal Studies, have been banging on about them for decades. But as more individuals have moved into running their own business, we’ve been hearing more about the real life case studies that push the complexity, inefficiency and unfairness of our tax system into the spotlight. The workforce changes have also grabbed politicians’ attention because they are creating a hole in the public finances.

The government has recently started to quantify the cost of giving lower taxes to an important and growing part of the workforce. There are lots of numbers out there, but here are the key official statistics.

HMRC estimate that the cost of giving lower rates of NICs to the self-employed relative to employees is £5.1bn, or £1,240 per self-employed person, in 2016/17. This is particularly striking since the total NICs paid by the self-employed is just £3bn. The cost of lower taxes for company owner managers is estimated to be even higher at £6bn, which equates to an average of £9,040 per company owner-manager. In both cases the averages masks the fact that most of the benefits are going to higher earning individuals. These costs are set to grow as the labour market continues to change. Most notably, the Office for Budget responsibility (OBR) has quantified the cost of growth in incorporations outstripping employment growth. They forecast that revenues will be £3.5bn lower in 2021/22 than if the small company population and employment grew at the same rate between now and then (assuming that the overall change in the size of the workforce remained the same). The government also expects to lose an additional £1bn of tax revenue as a result of further increases in self-employment.

The fact that the labour market is changing in ways that reduce tax revenues is a challenge for the government. Even if the chancellor (like others before him) was willing to overlook the distortions created by taxing different ways of working differently, the growing hole in the public finances requires action.

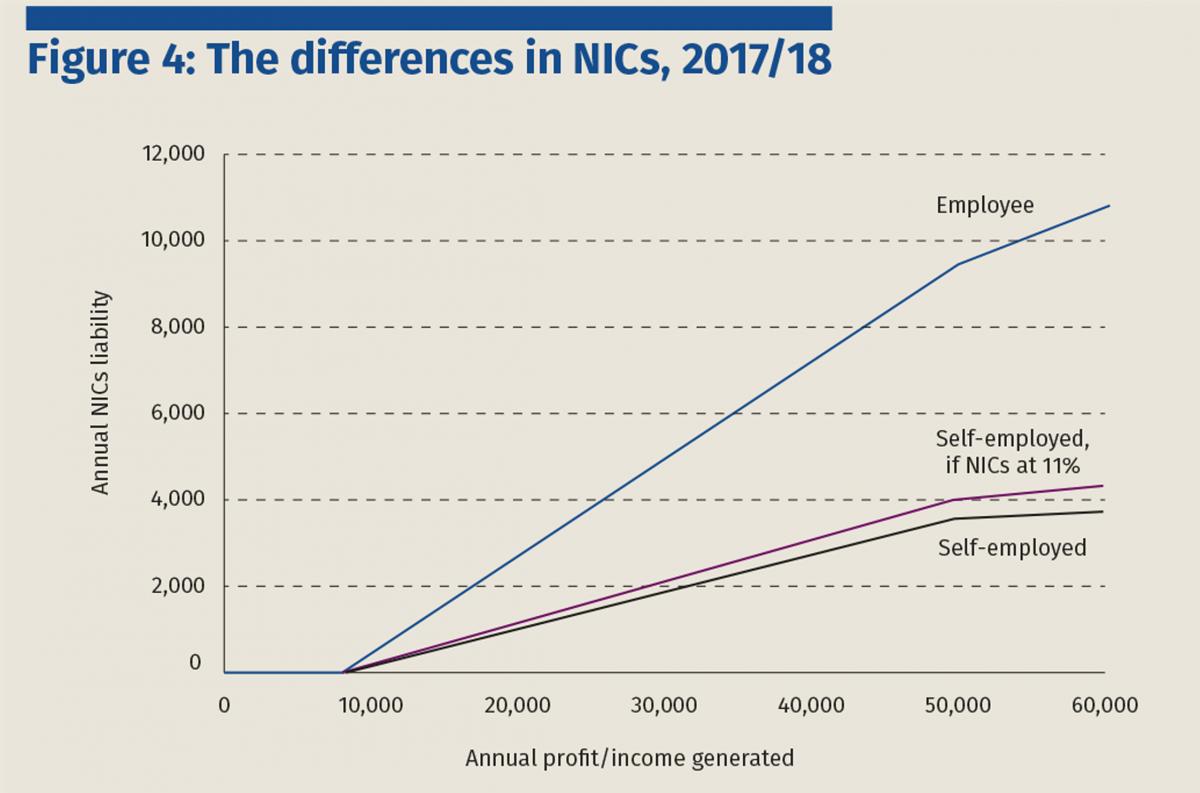

In fact, Philip Hammond cited concerns that ‘dramatically different treatment of two people earning essentially the same undermines the fairness of the tax system’ when announcing his plan to increase the main rate of self-employed NICs (class 4) from 9% to 11% in Budget 2017. This measure was due to raise £600m in 2020/21. He also announced a cut to the dividend tax allowance, which is due to raise £820m by 2020/21. Even had political pressure not forced a u-turn on the NICs measure, there would have still been a substantial hole in tax revenues by the end of the parliament. Raising self-employed NICs by two percentage points wasn’t going to plug the funding gap and was only a small step towards levelling the tax playing field for employees and the self-employed. This can be clearly seen in figure 4 (below), which shows the NICs schedules for employees and the self-employed in 2017/18, including the proposed rise to 11% for the latter. It is employer NICs, which should correctly be seen as a tax on a job that occurs through employment, that is driving the large wedge. The 9% main rate of NICs for the self-employed should be compared to a combined main rate on employees of 22.7%.

Despite the NICs u-turn, the chancellor clearly set out that he still judges the scale of the NICs difference between employees and the self-employed to be a problem and ‘continues to believe that’ reducing the tax difference ‘is the right approach’. The sentiment that something needs to be done is shared more widely. The current tax system is not a good answer to the question of how to tax different ways of working. The question we all face is how should the tax system be changed?

This is a tricky area. Any reforms must be mindful that the taxation of employees, the self-employed and company owner-managers sits exactly at the point where many parts of the tax system come together. Incentives to switch between legal forms depend on the bases and rates of income tax (including the treatment of dividends), NICs, corporation tax and capital gains tax. Changing any one of these has far-reaching effects: tax rates on earnings affect all employees, not just those who might otherwise set up a business; corporation tax affects all businesses, from one-man bands to multinationals; taxation of dividends and capital gains affects portfolio shareholders and buy-to-let landlords as well as business owner-managers. As such, the tax treatment of legal forms should always be seen in the context of the whole tax system.

The Mirrlees Review of the UK tax system undertaken at the IFS proposes a design for the whole tax system that aligns the taxation of income from different legal forms. It acknowledges that there are real differences between employees and individuals working for their own business. Importantly, the income of the latter can represent a mix of returns to labour effort and invested capital and this should be reflected in the tax treatment. But it also starts from the premise that the tax system should not favour one legal form over another without a very good reason for doing so (because of all the problems that creates). The proposed solution flows from these two principles and can be seen as comprising two parts. First, we should adjust the tax base to ensure that full allowances are given (at both personal and corporate tax levels) for the amounts saved and invested. There are various ways to achieve this but it would mean that the cost of investing in new equipment or of injecting equity into a new business, for example, would be fully tax deductible. This type of tax base is designed to avoid disincentives to save and invest.

Second, we should align the treatment of different legal forms by applying the same overall tax rate schedule to income derived from employment, self-employment and companies. Different income sources would still be subject to varying combinations of income tax, NICs, capital gains tax and corporation tax. But alignment would mean that an additional pound of income was taxed at the same rate regardless of how it was earned. Broadly, this could be achieved by: (i) aligning the NICs paid by self-employed individuals and those paid by employers and employees combined (preferably in the course of integrating NICs with personal income tax); and (ii) taxing dividend income and capital gains at the same rate schedule as earned income (including employee and employer NICs), with reduced tax rates for dividends and capital gains on shares to reflect corporation tax already paid. Note that alignment does not necessarily require an increase in the corporation tax rate, which would raise concerns around making the UK less competitive. Instead, overall rate alignment could be achieved at the personal level by adjusting dividend and capital gains tax rates while keeping a relatively low corporation tax rate. Note also that the prescription is for the alignment of tax rates and says nothing about the level. Alignment could be achieved through a combination of raising taxes on self-employment and cutting taxes on employment, if desired.

Reforming the tax base and aligning rates deals with the issues created by boundaries in the system by effectively removing the boundaries. This is distinct from policy solutions to date, almost all of which have tried to implement rules that refine what should fall on each side of the boundary (‘IR35’ rules are just one example). Since there will never be a clear dividing line between individuals based on their legal form, this approach is doomed to fail. Why then do we bother? If, instead, we removed the preferential treatment given to business owners, we would remove most concerns about how tax affects choices. Some problems would remain. For example, running your own business would still come with more opportunities for tax avoidance. But we would wipe out many distortions. This is preferable to living with the distortions provided by the current system, or patching it up in ways that simply move boundaries in the tax system or reduce one distortion at the expense of another.

One objection to this approach is the claim that it fails to recognise that lower rates should be used to encourage entrepreneurship and risk taking. It is important to recognise that the difficulty and risk associated with entrepreneurship do not in themselves justify favourable tax treatment. If the market does not provide sufficiently high rewards for such activities, they should not be undertaken. Preferential tax treatment may be justified if markets fail to provide the appropriate incentives for entrepreneurship. We may be concerned, for example, that too few new ideas will be tried out because innovators do not reap all of the rewards (some ‘spill over’ to other businesses that can learn from the experiences of the innovator). Or, we may worry that some small and/or new firms find it prohibitively expensive to raise external finance for their new ventures. But blanket reductions in tax rates for all the self-employed and company owner-managers are poorly targeted at alleviating such concerns. Most small businesses are not particularly innovative and do not generate significant spillover benefits to wider society. From newsagents to IT contractors, they consist of people quietly going about the (perfectly honourable) business of making a living by providing valuable goods and services to others – much as most ordinary employees do. Moreover, those individuals who get the lowest rates (for example, owner-managers who can afford to retain income in a company and access entrepreneurs’ relief) aren’t even necessarily those that are the most entrepreneurial. Even if there are some benefits that arise because some genuine entrepreneurs get lower taxes, there is little evidence that those gains are big enough to justify scattering tax benefits so widely and creating all of the problems associated with boundaries in the tax system.

To date, policies aimed at boosting entrepreneurship – including entrepreneurs’ relief, cuts to capital gains tax and various venture capital schemes – have been layered into the tax system with little thought about how they interact with previous policies or what precisely they are targeting. We should aspire to better designed policy responses to properly articulated policy aims. A level playing field is the correct benchmark against which to justify preferential treatment for one group or type of activity.

The NICs U-turn was a stark warning that substantially changing the tax system will not be easy. If the government can’t take a very small step towards aligning tax treatment, is there any hope that we’ll ever get a comprehensive solution?

We should all hope that the answer is yes. If we retain the current system we will allow the clear inequities and distortions it delivers to persist. The tax community may not be united in the exact details of how a good system would look, but there’s widespread agreement that the current system needs reform and growing agreement that we should do more than apply a few sticking plasters at the boundaries.

There are reasons for hope. The tax treatment of different ways of working is ripe for reform. The problems that have long been in the system aren’t going away. As more people move into self-employment and company owner-management, we should expect to see more attention being given to the issues around complexity, efficiency and fairness. The government will have to face the public finance consequences. If the government is unwilling to reform the taxation of the self-employed and owner-managers, they will have to find revenue elsewhere, increase borrowing or deliver further cuts to public spending. There aren’t any pain free options on the table.

Another reason for hope is that the challenge, while substantial, is less complex than many imagine. Our current system muddles many different issues together. The rules around how we tax income, the administration mechanisms we use to collect tax, access to publically funded benefits and the rights given through employment law are all knotted together into a largely incoherent mess. It doesn’t need to be like that. Each of these issues is important but they don’t all need to be tied together. If we can break away from this approach, we can start to look clearly at the aims of different policy levers and design policies accordingly. As more people come to see this, the challenge of implementing meaningful reform will appear less daunting.

A great first step towards reform would be for the government to set out a long-term vision for where the tax system is headed. That would still leave us with the substantial challenge of how to get from the current system to the end goal. But if we could agree on a broad vision, we could all work together to map out the pathway to reform. This could include working out packages of reforms, rather than focusing on individual measures. This has many merits. Changing any tax in isolation can be the policy equivalent of ‘whack-a-mole’: one particular problem is fixed, but at the expense of another one popping up elsewhere in the system. By creating packages we can minimise the new distortions created. Packages can also be designed in ways that prevent concentrated groups seeing large losses. Arguably, the government should have taken this approach when increasing class 4 NICs. In 2016, the self-employed were given a substantial boost to their pension entitlements. In April this year, class 2 NICs will be abolished. Increasing class 4 would probably have been more palatable had it been announced alongside the giveaways.

A similar opportunity may arise after Matthew Taylor publishes his review into employment practices in the modern economy this summer. This won’t cover tax issues, but it will almost certainly call for action in other related areas. If the government decides to extend some benefits to the self-employed (for example, parental benefits) they could team this with tax changes.

Ultimately, any reform worth doing will create losers. This is inevitable given that there is currently a large group of taxpayers who are receiving substantial benefits at the expense of others (including the 85% of the workforce who are employees). The losers will no doubt be more vociferous than the winners. This should not prevent us from fixing the tax system.